How to Compare Car Insurance Rates and Save Big in 2024

Shopping for car insurance can feel confusing. Many people pay more than they should because they do not compare rates. Insurance companies use different ways to decide how much you pay. Your age, where you live, what car you drive, and your driving history all affect your price.

If you want to save money and get the best coverage, you need to know how to compare car insurance rates the smart way.

The good news is, comparing car insurance rates does not have to be hard. With the right steps, you can quickly see which companies offer you the best deal. This guide will show you exactly how to do it, what to look for, and the common mistakes to avoid.

Whether you are buying insurance for the first time or thinking of switching providers, you will learn how to make a confident choice. You will also find out about hidden fees, how to read policy details, and tips most beginners miss.

Let’s break down the process so you can understand every part and make the best decision for your needs.

Understanding Car Insurance Rates

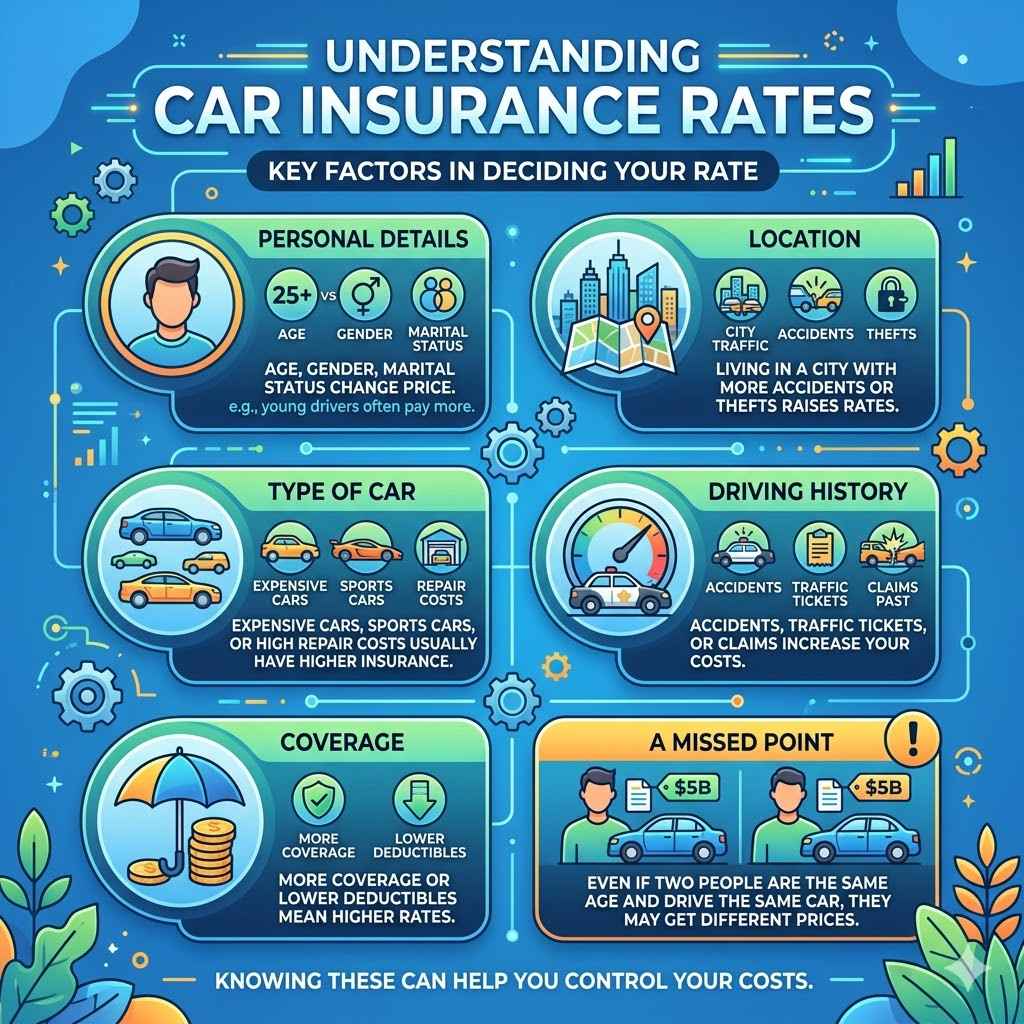

Before comparing rates, it helps to know what goes into them. Car insurance is not a fixed price. Companies look at many things to decide your rate. Knowing these can help you control your costs.

- Personal details: Your age, gender, and marital status can change your price. For example, young drivers often pay more.

- Location: Living in a city with more accidents or thefts can raise your rates.

- Type of car: Expensive cars, sports cars, or cars that cost more to repair will usually have higher insurance.

- Driving history: Accidents, traffic tickets, or claims in the past will increase your costs.

- Coverage: More coverage or lower deductibles mean higher rates.

One thing many people miss: even if two people are the same age and drive the same car, they may get different prices from different companies. This is because each company uses its own formula to judge risk.

Why Compare Car Insurance Rates?

Some drivers renew their policy with the same company every year. They may not realize that prices can change, and new discounts may appear. Here’s why comparing rates is important:

- Prices change: Insurance companies change their rates often. What was cheapest last year might not be now.

- Discounts differ: Some companies offer special deals for students, safe drivers, or bundling with home insurance.

- Coverage options: Not every policy covers the same things. You want to be sure you are protected.

- Service quality: Cheapest is not always best. Some companies pay claims faster or have better customer service.

A 2023 study by the National Association of Insurance Commissioners showed that U.S. drivers who compared rates saved an average of $390 per year. That’s real money in your pocket.

Steps To Compare Car Insurance Rates Effectively

To compare rates the right way, follow these steps. Each step helps you get accurate quotes and avoid surprises later.

1. Know What Coverage You Need

Start by deciding what kind of insurance you want. The main types are:

- Liability: Pays for damage or injury you cause to others. Required by law in most states.

- Collision: Pays for damage to your car from an accident.

- Comprehensive: Pays for damage not from an accident (like theft, fire, or hail).

- Personal injury protection (PIP): Covers medical costs for you and your passengers.

- Uninsured/underinsured motorist: Protects you if someone without enough insurance hits you.

Think about your car’s value, how much you drive, and your budget. If your car is old, you might skip collision and comprehensive to save money.

2. Gather Your Personal Information

Insurance companies will ask for details to give you quotes:

- Name, address, and date of birth

- Driver’s license number for each driver in your home

- Vehicle identification number (VIN) for each car

- Details about your driving history (accidents, tickets, claims)

- How many miles you drive per year

- How you use your car (work, school, leisure)

Having this ready speeds up the process and makes your quotes more accurate.

3. Decide On Deductibles And Limits

A deductible is what you pay out of pocket before insurance pays. Higher deductibles mean lower monthly costs, but you pay more if you have a claim. Policy limits are the maximum amount the company will pay. States have minimums, but you may want more for better protection.

For example, a common liability limit is $100,000 per person / $300,000 per accident. Many experts recommend these limits to avoid big bills after a serious crash.

4. Shop With Multiple Companies

Never settle for one quote. Compare at least three to five companies. Include:

- Large national brands (like Geico, Progressive, State Farm, Allstate)

- Regional or local companies (sometimes they offer lower rates)

- Online-only companies (these often have lower overhead and prices)

You can contact companies directly or use online comparison tools. Make sure to give the same information to each one.

5. Review Quotes Carefully

When you get quotes, look at more than just the price. Check:

- What is included and what is not

- Deductible amounts

- Coverage limits

- Extra features (like roadside assistance, rental car coverage)

- Discounts applied

Here is an example of how three different companies might compare for the same driver:

| Company | 6-Month Premium | Deductible | Liability Limits | Extras |

|---|---|---|---|---|

| Geico | $470 | $500 | 100/300/100 | Roadside |

| State Farm | $510 | $1,000 | 100/300/100 | Rental Car |

| Progressive | $485 | $500 | 100/300/100 | None |

Notice that the lowest price does not always mean the best value. State Farm has a higher deductible and includes a rental car. Geico is cheaper and includes roadside help.

6. Look For Discounts

Most insurance companies offer discounts, but you must ask or look for them. Common discounts include:

- Safe driver

- Multiple cars

- Bundling with home or renters insurance

- Good student

- Low mileage

- Military or senior

Sometimes, companies offer new discounts that others do not. For example, some give a discount for paying in full or using automatic payments.

7. Check For Hidden Fees And Exclusions

Some policies look cheap but have hidden fees or do not cover important things. Always ask:

- Is there a cancellation fee if I switch later?

- Are glass repairs covered?

- Does the policy cover rental cars?

- Are there restrictions for rideshare drivers (like Uber or Lyft)?

Read the fine print. If you do not understand something, ask.

8. Read Customer Reviews And Ratings

A low price is not good if the company is hard to work with. Look up customer reviews and ratings for claims service, speed, and fairness. Check trusted sources like J. D. Power, Consumer Reports, or the Better Business Bureau.

Here’s an example of customer satisfaction ratings:

| Company | Claims Satisfaction (out of 5) | Complaint Index |

|---|---|---|

| USAA | 4.8 | 0.25 |

| State Farm | 4.2 | 0.40 |

| Allstate | 3.9 | 0.65 |

A lower complaint index means fewer customer problems.

9. Consider Financial Strength

If you have a big claim, you want an insurance company that can pay. Check financial ratings from A. M. Best, Moody’s, or Standard & Poor’s. Most big companies are strong, but some smaller ones are not.

10. Watch Out For Short-term Deals

Some companies offer low rates for new customers but raise prices after the first year. Ask what your renewal rate might be and if there are any loyalty discounts for staying longer.

Common Mistakes When Comparing Car Insurance Rates

Even careful shoppers make mistakes. Avoid these to save money and headaches:

- Comparing different coverage levels: Always compare the same coverage and deductibles.

- Forgetting fees: Some policies add fees for monthly payments or changes.

- Not asking about discounts: Many discounts are not automatic.

- Ignoring customer service: Cheap insurance is not worth it if you cannot reach someone after an accident.

- Not checking renewal rates: Your rate may jump after the first term.

- Missing exclusions: Some policies do not cover things like custom parts or ridesharing.

- Not updating info: Giving wrong details can make your quote wrong, or even cancel your policy later.

How To Use Online Comparison Tools Wisely

Online tools make comparing fast, but be careful. Many tools are lead generators—they sell your info to many companies, and you may get spam calls. Use trusted sites (like NerdWallet, The Zebra, or directly from your state’s insurance department).

When using online tools:

- Double-check all info before submitting.

- Be ready for follow-up calls or emails.

- Do not give out your Social Security number unless you are ready to buy.

A smart tip: get quotes at the same time of day and week. Rates can change based on when you shop, especially near policy renewal periods.

Understanding The Impact Of Your Credit Score

In most states, your credit score affects your car insurance rate. Companies believe drivers with better credit file fewer claims. If your score is low, you may pay more—even if you have a clean driving record.

Some states (like California, Hawaii, and Massachusetts) do not allow credit scores to be used for insurance. Check your state’s rules.

If your credit improves, ask for a new quote. Many people forget this and overpay.

Comparing Car Insurance For Different Driver Profiles

Insurance rates change a lot based on your profile. Here is an example of how rates can differ:

| Driver | Age | Accidents | Annual Premium |

|---|---|---|---|

| Teen Driver | 18 | 0 | $3,600 |

| Adult Driver | 35 | 0 | $1,200 |

| Senior Driver | 70 | 1 | $1,950 |

Young drivers and seniors usually pay more. If you add a teen driver to your policy, always compare rates—some companies offer special discounts for families or students.

Key Insights Beginners Often Miss

- Timing matters: The best time to shop for new insurance is 30 days before your current policy ends. This gives you time to compare and avoid a gap in coverage.

- Bundling can save—but not always: Many companies offer discounts if you bundle car and home insurance. But sometimes, buying from two separate companies is still cheaper overall. Always compare both ways.

- Usage-based insurance: Some companies offer plans where your rate is based on how you drive. If you drive safely or less often, these plans can save you money.

- State differences: Each state has its own rules. Some require more coverage than others. Always check your state’s minimums and compare above that.

How To Switch Car Insurance After Comparing Rates

After you find a better deal, switching is easy:

- Apply for your new policy. Make sure it starts before your old one ends.

- Do not cancel your old policy until the new one is active.

- Tell your old company you want to cancel. Ask for a cancellation confirmation.

- Check for any refunds if you paid in advance.

- Print your new insurance card and keep it in your car.

A bonus tip: If you switch in the middle of your term, you may get a refund for unused time. But check for cancellation fees.

Special Cases: Comparing Car Insurance For Unique Needs

Not every driver fits the standard mold. Here are some special situations:

- Rideshare drivers: If you drive for Uber or Lyft, you need extra coverage. Some companies offer special rideshare policies. Standard insurance may not cover you while driving for work.

- Classic cars: Special insurance can be cheaper and give better coverage for old or collectible cars.

- High-risk drivers: If you have many tickets or accidents, your options may be limited. Look for companies specializing in high-risk insurance.

- New cars: Consider gap insurance. If your car is totaled, gap insurance pays the difference between what you owe and what the car is worth.

How Life Changes Affect Your Car Insurance Rate

Major life events can change your rates, sometimes in ways people do not expect:

- Moving: Rates can rise or fall a lot depending on your new ZIP code.

- Marriage: Married drivers often get lower rates.

- Divorce: Your rate may go up if you lose a multi-car or multi-policy discount.

- New job: If you drive less or can work from home, tell your insurer. Fewer miles can lower your rate.

- Kids getting a license: Shop around—adding a teen can double your premium, but some companies are much cheaper than others.

What To Do If You Are Denied Coverage

If a company refuses to insure you, do not panic. Some drivers are denied for too many accidents, tickets, or claims. If this happens:

- Ask why you were denied.

- Fix errors on your driving or claims record if possible.

- Look for companies that specialize in high-risk insurance.

- Check your state’s “assigned risk pool” program, which helps high-risk drivers get coverage.

Getting The Most Value From Your Car Insurance

It’s not just about finding the lowest price. Value means good coverage, fair service, and a price that fits your budget. Here’s how to get the most:

- Review your policy each year. Your needs may change.

- Ask your agent to check for new discounts.

- Raise your deductible if you have savings to cover it.

- Drop coverage you do not need (for example, on an old car).

- Keep your driving record clean.

Where To Find More Help

Your state’s insurance department can help if you have a complaint or need more information. They often have guides and rate comparisons for your area. For more detailed data, you can visit USA.gov’s state consumer resources.

Frequently Asked Questions

How Often Should I Compare Car Insurance Rates?

You should compare rates every year, or any time your life changes (like moving, marriage, or adding a driver). Rates can change often, and new discounts may appear.

Will My Credit Score Affect My Car Insurance Rate?

In most states, yes. A higher credit score usually means a lower insurance rate. Some states do not allow credit scores to be used, so check your state’s laws.

Can I Switch Insurance Companies Mid-policy?

Yes, you can switch anytime. Make sure your new policy starts before you cancel your old one. You may get a refund for unused time, but watch for cancellation fees.

What Information Do I Need To Get An Accurate Quote?

You need your driver’s license, vehicle information (VIN), driving history, and how much you drive. Having this ready makes quotes faster and more accurate.

Does Comparing Car Insurance Rates Hurt My Credit Score?

No. Getting quotes is a “soft inquiry” and does not affect your credit score. Only when you actually buy a policy might the company do a “hard pull,” but even then, the impact is small.

Comparing car insurance rates is one of the smartest ways to save money and get the right protection. With the steps and tips above, you can feel confident you are getting the best deal—without missing any important details.