How to Compare Car Insurance Quotes for Maximum Savings

Comparing car insurance quotes is one of the smartest steps you can take before choosing a policy. It’s not just about finding the lowest price—there are many factors that affect the real value of a policy. The right car insurance protects you, your car, and your finances, but picking the wrong one can leave you underinsured or paying too much.

Many people rush the process or get lost in technical terms, missing out on better deals or coverage. If you want to understand how to compare car insurance quotes the right way, you’re in the perfect place. This guide will walk you through each step, highlight what matters, and help you avoid common mistakes—even if you’re new to car insurance.

Why Comparing Car Insurance Quotes Matters

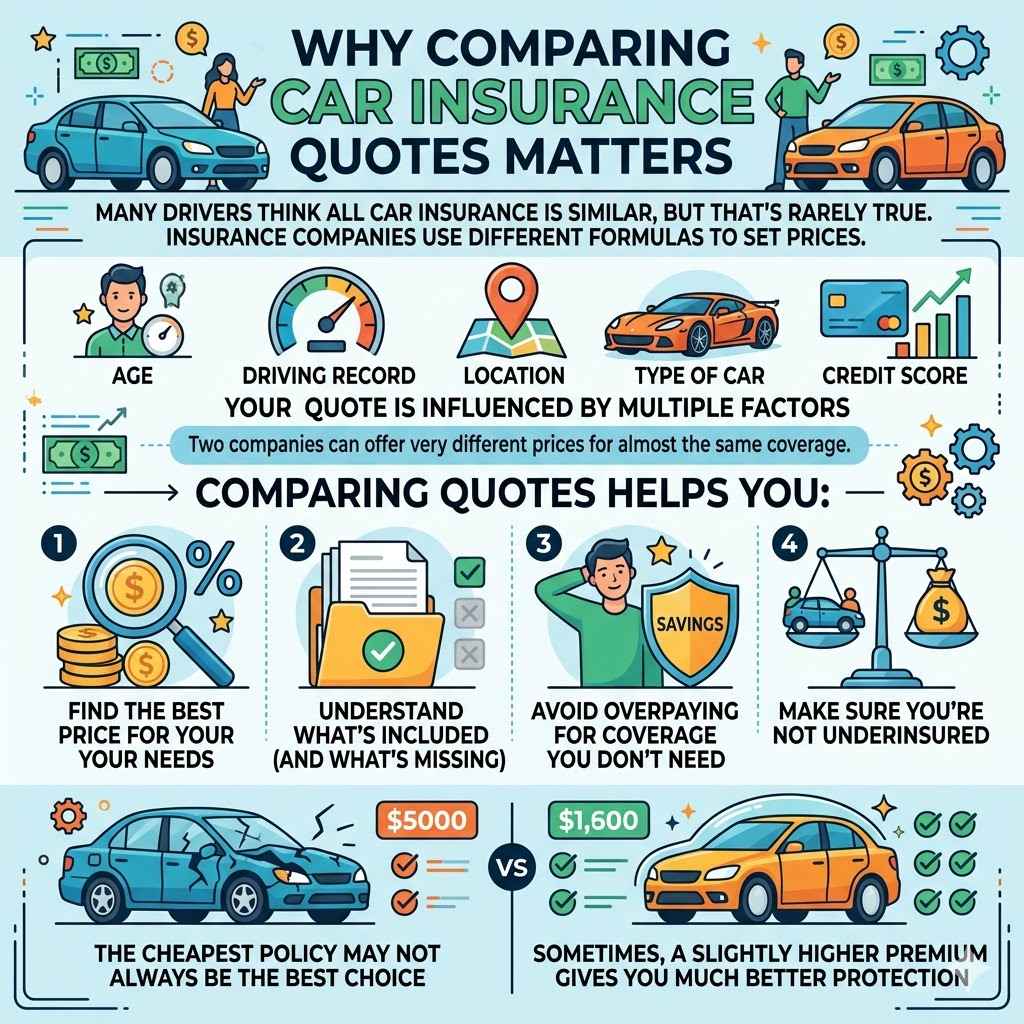

Many drivers think all car insurance is similar, but that’s rarely true. Insurance companies use different formulas to set prices. Your age, driving record, location, type of car, and even your credit score can change your quote. Two companies can offer very different prices for almost the same coverage.

Comparing quotes helps you:

- Find the best price for your needs

- Understand what’s included (and what’s missing)

- Avoid overpaying for coverage you don’t need

- Make sure you’re not underinsured

It’s easy to focus just on the monthly payment. However, the cheapest policy may not always be the best choice. Sometimes, a slightly higher premium gives you much better protection if an accident happens.

Key Factors That Affect Car Insurance Quotes

Before you compare, it helps to know what influences your quote. Here are the most important factors:

- Driver age and experience: Young or new drivers usually pay more.

- Driving history: Accidents, traffic tickets, and claims can raise your price.

- Location: Living in a busy city often means higher rates than a rural area.

- Type of car: Luxury, sports, or high-value cars cost more to insure.

- Coverage amount: Higher coverage means higher premiums.

- Deductibles: A higher deductible (what you pay before insurance kicks in) lowers your premium.

- Credit score: In many places, a better credit score means lower rates.

- Annual mileage: Driving more miles each year often increases your risk and your price.

- Claims history: Frequent claims can make insurers see you as higher risk.

Knowing how these factors work helps you understand why quotes differ and what changes you can make to get a better deal.

Types Of Car Insurance Coverage

Understanding the main types of coverage is essential before comparing quotes. Here are the common ones:

- Liability: Covers damage or injuries you cause to others.

- Collision: Pays for damage to your own car after an accident.

- Comprehensive: Protects against theft, weather damage, or hitting an animal.

- Personal injury protection: Helps with medical bills for you and your passengers.

- Uninsured/underinsured motorist: Covers you if the other driver doesn’t have enough insurance.

Some policies include extras like roadside assistance, rental car reimbursement, or glass coverage. Always read the details—small differences can matter a lot after an accident.

Steps To Compare Car Insurance Quotes Effectively

Jumping straight into price comparison can be a mistake. Here’s a step-by-step approach that ensures you get the right coverage at a fair price.

1. Gather Your Information

Insurance companies need details to give accurate quotes. Prepare the following:

- Your driver’s license number

- Car make, model, and year

- Vehicle Identification Number (VIN)

- How much you drive each year

- Where you park your car (garage or street)

- Details of any recent accidents or claims

Having this ready saves time and ensures you get the same quote from each company.

2. Decide What Coverage You Need

Think about your car’s value, how much you drive, and your risk level. If your car is old and not worth much, you might skip comprehensive or collision. If you lease or finance your car, the lender may require extra coverage.

Don’t just copy your current policy. Take this chance to see if your needs have changed.

3. Get Quotes From Multiple Companies

Never settle for just one or two quotes. Aim for at least 3–5. You can get quotes:

- Online, using insurance company websites or comparison tools

- By phone, speaking to agents directly

- Through insurance brokers, who work with several companies

When using online tools, be careful with your personal data. Only use trusted, secure sites.

4. Compare Apples To Apples

Make sure each quote is for the same type and amount of coverage. One company’s “basic” policy could be very different from another’s.

Here’s an example comparison:

| Company | Liability | Collision | Comprehensive | Deductible | Monthly Premium |

|---|---|---|---|---|---|

| Company A | $100,000 | $500 deductible | $500 deductible | $500 | $95 |

| Company B | $100,000 | $1,000 deductible | $1,000 deductible | $1,000 | $85 |

| Company C | $100,000 | $500 deductible | $500 deductible | $500 | $110 |

Notice how Company B is cheaper, but the deductibles are higher, meaning you’ll pay more out of pocket if you have a claim.

5. Look Beyond Price

The cheapest quote is tempting, but other factors matter:

- Claims process: How easy is it to file and track a claim?

- Customer service: Are agents available and helpful?

- Financial strength: Will the company be able to pay claims?

- Extra features: Roadside assistance, accident forgiveness, new car replacement, etc.

Check company reviews, ratings, and complaint records. A policy is only good if the company stands behind it when you need them.

6. Understand Discounts

Most insurers offer discounts that can lower your premium:

- Good driver (no accidents or tickets)

- Multi-policy (bundle with home or renters insurance)

- Good student (for young drivers)

- Anti-theft devices

- Low annual mileage

- Paying in full (instead of monthly)

Ask each company what discounts you qualify for. Some discounts aren’t advertised on websites, so it’s worth asking an agent directly.

7. Read The Fine Print

Always review the policy documents before buying. Watch out for:

- Exclusions (what’s not covered)

- Limits on rental cars or repairs

- Penalties for late payments

- Cancellation terms

Two policies might look similar in price and coverage, but the fine print can hide big differences.

8. Consider The Deductible

A higher deductible lowers your monthly premium, but you’ll pay more if you have an accident. Choose a deductible you can afford in an emergency.

Here’s how deductibles change your premium:

| Deductible | Monthly Premium | Out-of-Pocket Cost After Accident |

|---|---|---|

| $500 | $95 | $500 |

| $1,000 | $85 | $1,000 |

| $2,000 | $75 | $2,000 |

Don’t pick a high deductible just to save money unless you’re sure you can cover it if needed.

9. Check For Add-ons And Special Coverages

Sometimes, you need more than the basics. Add-ons can include:

- Roadside assistance

- Rental car coverage

- Gap insurance (for leased cars)

- Glass repair

- Accident forgiveness

These extras usually cost more, but they can be worth it for peace of mind. Make sure to compare these options between companies.

10. Review Payment Options

Some companies offer better deals if you pay in full instead of monthly. Others have flexible options like automatic payments, which can also qualify you for a discount. Late payment fees or strict payment schedules can be a problem if you have cash-flow issues.

11. Consider Company Reputation And Support

A good insurance company is more than just a price. Research:

- How easy it is to reach customer service

- How claims are handled (speed, fairness)

- Company financial ratings (look for A or better from agencies like AM Best)

- Customer complaint history (available on government websites)

Websites like the National Association of Insurance Commissioners track complaint ratios, which can highlight companies with poor service.

12. Re-evaluate Regularly

Your needs change over time. Maybe you bought a new car, moved, or your credit score improved. It’s a smart idea to shop for new quotes every year or after big life changes. Even a small change can save you hundreds of dollars.

Common Mistakes When Comparing Car Insurance Quotes

Many drivers make simple mistakes that cost them money or leave them at risk. Here are some to watch out for:

- Focusing only on price: Cheap policies often have poor coverage or high deductibles.

- Not matching coverage: Comparing different coverage amounts or types is misleading.

- Ignoring exclusions: Not all policies cover the same things. Always check.

- Missing discounts: Not asking about available discounts leaves savings on the table.

- Not checking company reputation: A low price is worthless if the company has bad service.

- Failing to update details: Quotes are only accurate if your info is up to date.

- Not reading the fine print: Surprises in policy terms can be expensive.

- Assuming loyalty pays: Staying with the same insurer doesn’t always mean better rates.

Examples: Comparing Two Realistic Quotes

Let’s break down a sample comparison. Imagine two companies offer you these quotes:

| Feature | Company X | Company Y |

|---|---|---|

| Liability Coverage | $100,000 | $100,000 |

| Collision Deductible | $500 | $1,000 |

| Comprehensive Deductible | $500 | $1,000 |

| Monthly Premium | $110 | $95 |

| Rental Car Coverage | Included | Not Included |

| Customer Rating | 4.5/5 | 4.0/5 |

At first glance, Company Y looks cheaper. But it has higher deductibles and no rental car coverage. If you need a rental after an accident, Company X could actually save you money and hassle.

Non-obvious insight: The real cost of insurance isn’t just the premium—you must also consider what you’ll pay in different situations, like accidents or theft.

How To Get The Most Accurate Quotes

To avoid surprises, always:

- Use accurate, up-to-date information about yourself and your car

- Be honest about your driving history and claims

- Use the same coverage levels when requesting quotes

- Double-check your details before submitting forms

Some people try to hide tickets or accidents to get a better quote, but insurance companies will find out. Inaccurate info can void your policy or lead to denied claims.

How Technology Makes Comparing Easier

Today, many online tools and apps let you compare multiple quotes in minutes. Some let you adjust coverage options and see instant price changes. This is helpful, but be careful:

- Some sites sell your info to many insurers, leading to lots of sales calls.

- Not all companies are on every comparison tool.

- Some quotes may be “estimates” and not final prices.

For the most accurate results, use a mix of direct company websites and well-known comparison tools. Check privacy policies before entering personal details.

What To Do After You Choose A Policy

Once you pick your policy:

- Confirm all coverage details in writing.

- Set up your payment method and schedule.

- Cancel your old policy only after the new one is active.

- Print or download your proof of insurance.

- Review your policy every year, or after big life changes.

If you have questions, call the insurance company and ask. Good companies will be happy to help.

Tips For Special Cases

Car insurance isn’t one-size-fits-all. Here are some situations that need extra care:

- Teen drivers: Adding a teen to your policy is expensive, but discounts for good grades or driver training can help.

- High-value cars: Choose higher limits and comprehensive coverage. Some insurers specialize in luxury vehicles.

- Low-mileage drivers: Some companies offer “pay-per-mile” insurance, which can save you money if you drive very little.

- Rideshare drivers: If you drive for Uber or Lyft, you need special coverage or a rideshare add-on.

- Non-owner insurance: If you don’t own a car but drive sometimes, non-owner insurance is cheaper and keeps you covered.

How State Laws Affect Car Insurance

Each state or country has its own minimum requirements for car insurance. For example, most U. S. states require liability insurance, but the minimum amount varies. Some states also require personal injury protection or uninsured motorist coverage.

Always check your local laws before buying a policy. Not having enough coverage can lead to fines, license suspension, or paying out of pocket after an accident.

For more on state insurance laws, you can visit the National Association of Insurance Commissioners.

Frequently Asked Questions

What Is The Best Way To Compare Car Insurance Quotes?

The best way is to get quotes from at least three reputable companies for the same coverage amounts and deductibles. Use both online tools and company websites. Always check coverage details, discounts, and company reputation—not just price.

How Often Should I Compare Car Insurance Quotes?

Compare quotes every year, or any time your situation changes (new car, moving, adding a driver). Insurance rates change often, and you may qualify for new discounts.

Do All Insurance Companies Offer The Same Coverage?

No. While basic coverage types are similar, each company offers different extras, exclusions, and limits. Always read the details and compare carefully.

Will Comparing Quotes Hurt My Credit Score?

No. Getting insurance quotes usually uses a “soft pull” of your credit, which doesn’t affect your score. Only applying for a loan or credit card does a “hard pull. ”

What If I Find A Cheaper Quote After Buying A Policy?

You can switch insurers at any time. Just make sure your new policy is active before canceling the old one to avoid gaps in coverage. Check for cancellation fees in your current policy.

Comparing car insurance quotes isn’t just about saving money—it’s about protecting yourself, your family, and your future. With a careful, step-by-step approach, you can find the right coverage, avoid common traps, and drive with confidence knowing you’re well protected.