How Much is a Honda Civic Monthly Payment? (2025 Cost Guide)

Shopping for a new car can be exciting, but it often raises one big question: how much will the monthly payment really be? The Honda Civic is a favorite for many drivers around the world, thanks to its reliability, modern features, and affordable price. But figuring out your actual monthly cost is not always simple. Many things can change your payment, from the car’s price to your loan details and even where you live.

If you are thinking about buying or leasing a Honda Civic, this guide will help you understand everything that affects your monthly payment. We will look at real examples, loan and lease options, and tips to keep your payment low.

Whether you are buying your first car or want to upgrade, this article will give you the knowledge to plan your budget with confidence.

Main Factors Affecting Honda Civic Monthly Payment

When you see a car price in an ad, you might think that is what you pay each month. But the monthly payment depends on many things besides the sticker price. Here are the main factors:

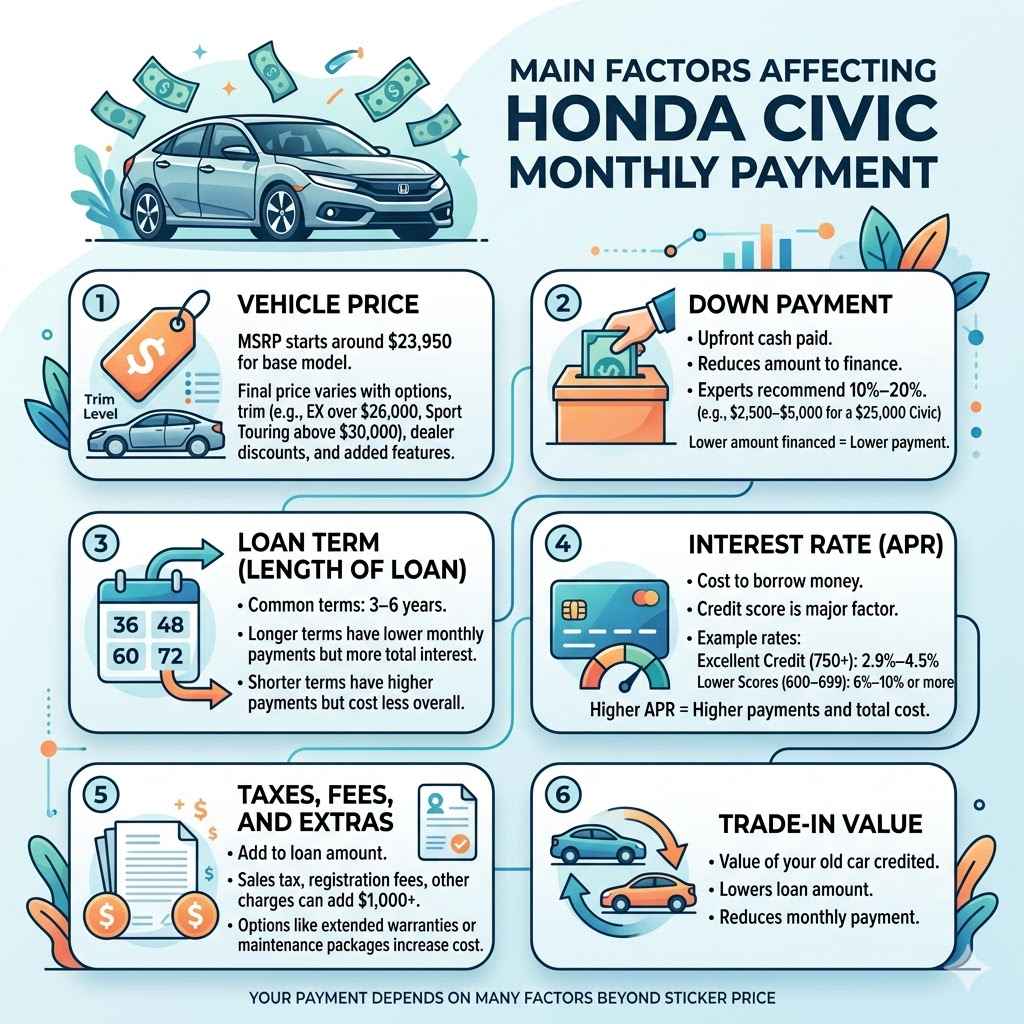

1. Vehicle Price

The MSRP (manufacturer’s suggested retail price) of a new Honda Civic usually starts around $23,950 for the base model in the U.S. However, most buyers do not pay exactly this price. The final price can be higher or lower depending on options, trim level, dealer discounts, or added features.

For example, a Honda Civic EX with more features can cost over $26,000. If you choose the Sport Touring trim, it could go above $30,000.

2. Down Payment

The down payment is the cash you pay upfront when you buy the car. A higher down payment reduces the amount you need to finance, which lowers your monthly payment. Most experts recommend putting down at least 10%-20% of the car’s price. For a $25,000 Civic, that means $2,500–$5,000.

3. Loan Term (length Of Loan)

The loan term is how long you take to pay back the loan. Common lengths are 36, 48, 60, or 72 months (3–6 years). A longer loan term means lower monthly payments, but you will pay more in total interest over time. Shorter terms have higher payments but cost less overall.

4. Interest Rate (apr)

The annual percentage rate (APR) is the interest you pay to borrow money for the car. Your credit score is the biggest factor in your rate. For example, excellent credit (750+) may get you rates as low as 2.9%–4.5%, while lower scores (600–699) may see rates from 6%–10% or more. The higher the rate, the more you pay each month and in total.

5. Taxes, Fees, And Extras

Car buyers also pay sales tax, registration fees, and other charges. These can add $1,000 or more to your loan amount. Some buyers add options like extended warranties or maintenance packages, increasing their monthly cost.

6. Trade-in Value

If you trade in your old car, the dealer gives you credit toward your new Honda Civic. This trade-in value lowers the loan amount, reducing your payment.

Example: Calculating Honda Civic Monthly Payments

Let’s see how these factors come together in a real-world example. Imagine you want to buy a new Honda Civic EX:

- Price: $26,000

- Down Payment: $3,000

- Loan Term: 60 months (5 years)

- Interest Rate: 5%

- Sales Tax and Fees: $1,500

First, subtract the down payment from the car price:

$26,000 – $3,000 = $23,000

Add taxes and fees:

$23,000 + $1,500 = $24,500

Now, you finance $24,500 for 60 months at 5% APR.

Using a basic auto loan calculator, the monthly payment is about $462.

If you trade in a car worth $2,000, your financed amount drops to $22,500, and your monthly payment goes down to about $425.

How Monthly Payments Change With Different Loan Terms

The length of your loan makes a big difference. A shorter loan means higher payments, but you pay less interest overall. Here’s a quick comparison for a $25,000 loan at 5% APR:

| Loan Term | Monthly Payment | Total Interest Paid |

|---|---|---|

| 36 months | $749 | $1,970 |

| 48 months | $576 | $2,634 |

| 60 months | $472 | $3,321 |

| 72 months | $402 | $3,929 |

You can see that longer loans mean lower monthly payments but much more interest paid in total.

Impact Of Credit Score On Honda Civic Monthly Payment

Your credit score is one of the most important factors. Lenders use it to decide your interest rate. Here’s how much it can change your Civic payment:

Assume you borrow $25,000 for 60 months.

| Credit Score Range | Estimated APR | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| 750+ | 3.5% | $455 | $2,287 |

| 700–749 | 4.5% | $466 | $2,953 |

| 650–699 | 6.5% | $490 | $4,433 |

| 600–649 | 9.5% | $525 | $6,527 |

| 550–599 | 13.5% | $576 | $9,567 |

A lower credit score can add over $100 per month to your payment.

Buying Vs. Leasing A Honda Civic

Many people ask if leasing a Civic is cheaper than buying. The answer depends on your goals.

Buying

When you buy, you pay off the car and keep it. Monthly payments are usually higher than leasing, but you own the car at the end.

Leasing

Leasing means you pay to use the car for 2–3 years, then return it. Monthly payments are often lower because you only pay for the car’s depreciation (how much value it loses), not the full price. Most leases have mileage limits (e.g., 12,000 miles per year). If you go over, you pay extra fees.

Example: Lease Vs. Buy Payment

Suppose you want a 2024 Honda Civic Sport (MSRP $25,000):

- Lease: $2,000 down, 36 months, $310/month, 12,000 miles/year

- Buy: $2,000 down, 60 months at 5% APR, $435/month

Leasing saves you about $125 per month, but you won’t own the car.

Other Costs To Consider

Your monthly payment is not the only cost. Owning a car includes:

- Insurance: Honda Civics are usually less expensive to insure than SUVs or trucks, but rates vary by location, driver age, and history.

- Fuel: Civics are fuel-efficient. The 2024 model gets around 31 mpg city/40 mpg highway.

- Maintenance: Civics are reliable, but oil changes, tires, and brakes still add up.

- Registration and Taxes: These can be paid yearly or rolled into your loan.

Comparing Honda Civic Payments To Other Cars

How does the Civic’s monthly payment stack up to similar cars? Here’s a comparison:

| Car Model | Price | Estimated 60-Month Payment @ 5% APR |

|---|---|---|

| Honda Civic LX | $23,950 | $452 |

| Toyota Corolla LE | $22,050 | $416 |

| Hyundai Elantra SE | $21,625 | $408 |

| Volkswagen Jetta S | $21,435 | $404 |

| Kia Forte LXS | $20,815 | $393 |

The Civic is a bit more expensive than some rivals, but many buyers believe its quality and resale value make up for it.

How To Lower Your Honda Civic Monthly Payment

Paying less per month means more money for other things. Here are smart ways to reduce your payment:

- Increase your down payment. Even $1,000 more can make a noticeable difference.

- Shop for a lower interest rate. Get pre-approval from banks or credit unions, not just the dealer.

- Choose a base model. Higher trims and extras add thousands to the price.

- Consider certified pre-owned (CPO). A lightly used Civic can save you $5,000 or more.

- Shorten the loan term if you can afford it. You will pay more monthly, but less in interest overall.

- Look for manufacturer incentives. Honda sometimes offers special deals or low APRs.

- Trade in your old car. The value can reduce your loan amount.

Common Mistakes When Financing A Honda Civic

Many buyers focus on the monthly payment alone. Here are mistakes to avoid:

- Ignoring the total cost. A lower payment with a longer loan means more interest.

- Not checking your credit. Always know your score and try to improve it before buying.

- Rolling in negative equity. If you owe more than your trade-in is worth, adding the difference to your new loan increases your payment.

- Skipping the fine print. Some loans have prepayment penalties or other fees.

- Underestimating insurance and taxes. Get quotes before you sign.

Real-world Payment Examples

To help you see what a Honda Civic might cost per month, here are examples from real buyers:

- Mia, Texas: Bought a new 2023 Civic Sport for $25,500. Put down $4,000, financed $23,000 for 60 months at 4%. Payment: $424/month.

- James, California: Leased a 2024 Civic EX for 36 months, $2,500 down, $315/month, 10,000 miles per year.

- Ava, Florida: Bought a certified pre-owned 2021 Civic for $19,900 with $3,000 down, 60 months at 6%. Payment: $325/month.

These examples show how location, down payment, and loan terms change the payment.

Special Offers And Incentives

Honda and its dealers often provide special financing offers. These can include:

- Low APR loans: Sometimes as low as 1.9% for qualified buyers.

- Cash rebates: Direct discounts on the car.

- Lease specials: Lower payments with extra mileage or less money down.

Always ask about current deals before you commit. Offers can change monthly and by region. You can check the latest incentives on the official Honda Special Offers page.

Should You Buy New, Used, Or Lease?

Each option changes your monthly payment:

New

New Civics cost more, but you get the latest features, warranty, and lower maintenance early on. Payments are highest.

Used

Buying used or certified pre-owned lowers the price and payment, but the car may have more miles and less warranty.

Lease

Leasing has the lowest payment, but you do not own the car at the end. Good for people who want a new car every few years and drive less.

Non-obvious Insights

- Factory-to-dealer incentives are sometimes not advertised. Ask the dealer if there are extra discounts.

- Gap insurance can be rolled into your loan payment. This covers you if your car is totaled and you owe more than insurance pays.

- End-of-lease costs can surprise people: Things like excess wear or mileage fees can add hundreds to your last payment.

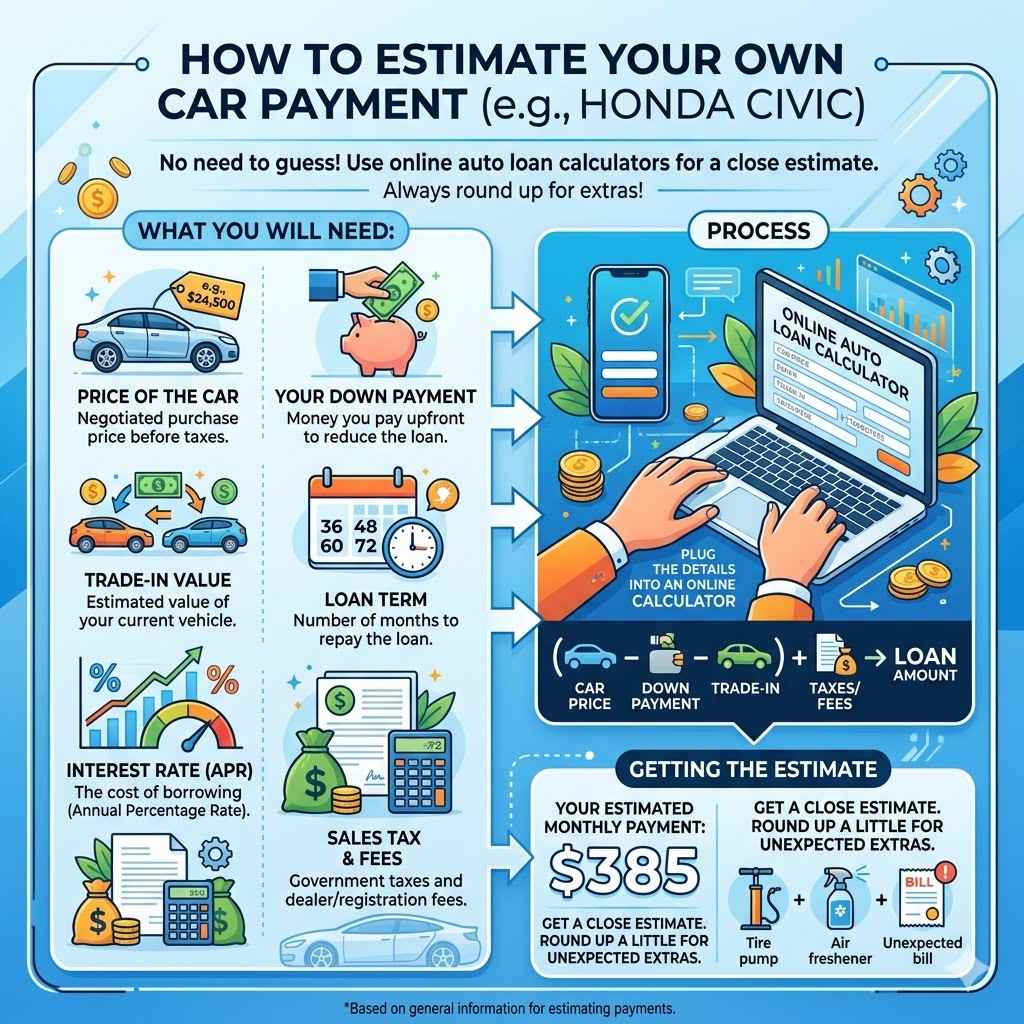

How To Estimate Your Own Payment

You do not need to guess. There are many auto loan calculators online. To estimate your Honda Civic monthly payment, you will need:

- Price of the car

- Your down payment

- Any trade-in value

- Loan term (number of months)

- Interest rate (APR)

- Sales tax and fees

Plug these into a calculator to get a close estimate. Always round up a little for extras you might not expect.

Frequently Asked Questions

What Is The Average Monthly Payment For A New Honda Civic?

The average monthly payment for a new Honda Civic in 2024 is between $400 and $500 for a 60-month loan, with a typical down payment and average credit score. Payments can be lower or higher depending on your location, loan terms, and credit.

Is It Better To Lease Or Buy A Honda Civic To Save Money?

Leasing often gives you a lower payment, but buying is usually better in the long run if you keep the car more than 3–5 years. Leasing is good if you want a new car often and do not drive many miles.

How Much Should I Put Down On A Honda Civic?

A good down payment is 10%–20% of the car’s price. For a $25,000 Civic, that means $2,500–$5,000. More money down means a lower loan and lower payments.

Can I Get A Honda Civic With Bad Credit?

Yes, but your interest rate will be much higher, and your monthly payment can be $100 or more above someone with good credit. Improving your credit score before buying can save you thousands.

What Extra Costs Are Not In The Monthly Payment?

Your payment usually does not include insurance, maintenance, yearly registration, or extra options like extended warranties. Always add these to your budget.

The Honda Civic remains one of the best choices for an affordable, reliable vehicle. Understanding how your monthly payment is calculated helps you get the best deal and avoid surprises. With the tips and insights in this guide, you can make a smart choice and drive with confidence.