How to Compare Car Insurance Prices: Save Big on Your Policy

Finding the right car insurance can feel complicated. Prices change from company to company, and each policy has its own rules. If you don’t compare carefully, you might pay more than you should, or miss out on important coverage. The good news?

Comparing car insurance prices is not as hard as it seems. With a step-by-step approach, you can save money and get the protection you need. This article will guide you through everything—from understanding what affects price, to using comparison tools, to avoiding mistakes that trap beginners.

You’ll also see real examples and answers to common questions, so you can compare car insurance prices confidently.

Why Car Insurance Prices Vary

Car insurance prices are not the same for everyone. Even if two people drive the same car, their costs can be very different. Insurance companies look at many factors when they decide your price. Here are some of the main reasons:

- Personal history: Your driving record, claims, and age matter.

- Car details: The make, model, and age of your car affect the risk.

- Location: Where you live can change prices. Busy cities often cost more.

- Coverage type: More coverage means higher prices.

- Discounts: Some companies offer special discounts.

Let’s look at each factor more closely.

Personal History

If you have a clean driving record, you usually get a lower price. Drivers with accidents or speeding tickets often pay more. Age also matters. Young drivers (under 25) are seen as risky, so their prices are higher. Older drivers, especially those over 60, sometimes pay less.

Car Details

Expensive cars cost more to insure. If your car is new, insurance is often higher because repairs are costly. Cars with safety features or anti-theft devices can get discounts.

Location

If you live in a city with lots of traffic or theft, your price may be higher. Rural areas usually see lower prices. Some states or countries have different rules for insurance, which changes the cost.

Coverage Type

There are different types of coverage:

- Liability: Pays for damage you cause to others.

- Collision: Covers your car if you hit something.

- Comprehensive: Protects against theft, fire, or weather.

- Personal injury protection: Pays for medical costs.

Choosing more coverage increases your price, but gives you better protection.

Discounts

Many companies offer discounts for things like:

- Safe driving

- Bundling home and car insurance

- Being a student

- Having safety features

Always ask about discounts when comparing.

Steps To Compare Car Insurance Prices

Comparing car insurance prices is not just about looking at numbers. You need to check what’s included, what’s excluded, and how it fits your needs. Here’s a clear guide:

- Know What You Need

- Collect Your Personal Information

- Use Online Comparison Tools

- Check Coverage Levels

- Look for Discounts

- Read the Fine Print

- Ask Questions

- Compare Customer Service

- Review Company Reputation

- Make Your Decision

Let’s break down each step.

1. Know What You Need

Before you compare, decide what type of coverage you want. Some people only need liability insurance. Others want full protection, including collision and comprehensive. If your car is new or valuable, more coverage is smart. If your car is old and not worth much, basic coverage may be enough.

Think about your risks. Do you live in a flood area? Is theft common in your city? How much can you afford to pay out-of-pocket if you have an accident? List your needs before you start.

2. Collect Your Personal Information

Insurance quotes are based on your details. Gather:

- Your driver’s license number

- Car registration

- List of past accidents or claims

- Your home address

- Your car’s make, model, and year

Having this information ready saves time and helps you get accurate prices.

3. Use Online Comparison Tools

Many websites let you compare prices quickly. You enter your details, and they show quotes from different companies. These tools are good for seeing a range of prices, but remember: not all companies are included.

Some well-known comparison sites are NerdWallet, The Zebra, and Compare.com. Use more than one site for a better view. You can also visit insurance company websites directly.

A common beginner mistake is to rely only on the first site they try. Prices can change, so check several sources.

4. Check Coverage Levels

Don’t just look at the price. Check what coverage each policy offers. Some quotes are cheap because they cover less. Look for:

- Limits: How much the company will pay per accident.

- Deductibles: The amount you pay before insurance starts.

- Exclusions: What the policy does NOT cover.

Compare apples to apples. If one quote is $500 and another is $650, but the second covers twice as much, it may be a better deal.

5. Look For Discounts

Discounts can save you a lot. Not all companies show discounts in their quotes. Ask about:

- Multi-policy discounts (bundle home and car)

- Good driver discounts

- Student discounts

- Safe car discounts

- Military or senior discounts

A non-obvious tip: Some companies offer hidden discounts for things like paying annually instead of monthly. Ask about all options.

6. Read The Fine Print

Insurance contracts are full of details. Read the terms. Look for:

- Cancellation fees

- Payment rules

- Claim process

- Renewal terms

Some companies have low prices but high fees for changes or claims. Don’t skip this step.

7. Ask Questions

If something is unclear, ask. You can call the insurance company or chat online. Good questions include:

- What is covered in this price?

- Are there extra fees?

- How does the claims process work?

- Are there limits for certain types of accidents?

Asking questions helps you avoid surprises later.

8. Compare Customer Service

Price is important, but service matters too. If you have an accident, you want help fast. Check:

- How easy is it to contact the company?

- Are claims processed quickly?

- Do customers give good reviews?

Poor service can cost you more in the long run. Look for companies with strong support.

9. Review Company Reputation

Some companies are more reliable than others. Search online for reviews, or ask friends and family. Look for:

- Financial strength (can the company pay claims?)

- Long history in the business

- Awards or recognition

You can check ratings at places like AM Best or J.D. Power. This step is often missed by beginners, but it’s crucial.

10. Make Your Decision

After you compare prices, coverage, discounts, and reputation, choose the policy that fits your needs and budget. Don’t rush. Take time to review everything.

Real Example: Comparing Two Policies

Let’s compare two sample car insurance policies. You will see how prices and coverage can differ.

| Company | Annual Price | Coverage | Deductible | Discounts |

|---|---|---|---|---|

| SafeDrive Insurance | $720 | Liability + Collision | $500 | Safe driver, bundled policy |

| BudgetAuto | $540 | Liability only | $1,000 | Student discount |

The cheaper policy ($540) covers less, and has a higher deductible. If you have an accident, you pay more out-of-pocket. The $720 policy costs more, but offers broader protection and lower deductible. Which is better? It depends on your needs.

Comparing Coverage Types

Not all policies cover the same risks. Here’s a simple comparison of common coverage types:

| Coverage Type | What It Covers | Typical Cost Impact |

|---|---|---|

| Liability | Damage to others | Lowest price |

| Collision | Your car if you hit something | Medium price |

| Comprehensive | Theft, fire, weather | Higher price |

| Personal Injury Protection | Medical costs for you | Varies |

Adding more coverage increases price. Decide what risks matter most to you.

Mistakes To Avoid When Comparing Car Insurance

Many people make mistakes when comparing car insurance prices. Avoid these traps:

- Comparing only price: Cheap isn’t always best. Check coverage.

- Ignoring deductibles: High deductibles mean you pay more in an accident.

- Missing discounts: Always ask about possible savings.

- Skipping the fine print: Extra fees can surprise you.

- Trusting only online reviews: Some reviews are fake. Check several sources.

- Not updating personal info: Wrong info can make quotes inaccurate.

- Choosing the first option: Look at several policies before deciding.

A non-obvious insight: Policies sometimes change when you buy. Always confirm the final contract matches the quote.

Using Comparison Websites Vs. Agent

There are two main ways to compare car insurance prices: online websites and insurance agents.

Online Comparison Sites

Online sites are fast and easy. You see many prices at once. You don’t need to talk to anyone. But, not every company is listed, and sometimes prices are estimates.

Insurance Agents

Agents can give advice based on your needs. They may find special deals or explain complex rules. You can ask questions and get help with paperwork. The downside? Agents may represent only a few companies.

Which is better? Use both. Start online to see the range, then talk to an agent for details.

Data: Average Car Insurance Prices

Knowing the average price helps you spot good deals. According to the National Association of Insurance Commissioners, the average annual car insurance price in the United States is about $1,070 for basic coverage. Prices can be higher in cities and lower in rural areas.

Here’s a comparison of average prices by state:

| State | Average Annual Price |

|---|---|

| California | $1,200 |

| Texas | $1,050 |

| Florida | $1,450 |

| Ohio | $900 |

Prices change based on your city, driving record, and other factors.

How To Save Money On Car Insurance

Comparing prices is just one part. You can also lower your cost by:

- Raising your deductible (but be ready to pay more in an accident)

- Bundling home and car insurance

- Improving your credit score

- Driving safely (no accidents or tickets)

- Asking about special offers

A tip for beginners: Many companies lower your price if you take a safe driving course. Ask your insurer if they offer this.

What To Do After You Choose

Once you pick a policy:

- Confirm your details are correct.

- Read the contract carefully.

- Ask about payment options (monthly, yearly).

- Keep proof of insurance in your car.

- Review your policy each year. Prices and needs change.

If you change cars or move, update your insurance right away.

The Role Of Deductibles

A deductible is the amount you pay before insurance helps. If your deductible is $500, and you have a $2,000 accident, you pay $500, and insurance pays $1,500.

Lower deductibles mean higher prices, but you pay less if something happens. Higher deductibles save money, but increase your risk. Choose the amount that fits your budget.

How Car Insurance Companies Set Prices

Insurance companies use math and data to set prices. They look at:

- Your age and gender

- Driving history

- Type of car

- Where you live

- Claims history

They use statistics to predict risk. For example, young male drivers are seen as high risk, so prices are higher.

Some companies use telematics devices to track your driving. If you drive safely, you can get discounts.

Comparing Extras And Add-ons

Some policies include extras. These can be useful, but add to the price. Look for:

- Roadside assistance

- Rental car coverage

- Glass repair

- Accident forgiveness

Decide if you need these add-ons. Sometimes they are worth the cost, sometimes not.

Comparing For Families Vs. Individuals

If you have a family, look for policies that cover multiple drivers and cars. Family policies often include discounts. For individuals, check if the policy fits your lifestyle. If you drive rarely, ask about low-mileage discounts.

International Comparison

Car insurance prices and rules change by country. For example, in the UK, average prices are about £470 per year. In Australia, prices range from AU$700 to AU$1,500.

Always check local rules when comparing. Some countries require certain types of coverage by law.

For more details on global insurance standards, you can visit Wikipedia.

Updating Your Policy

If your life changes, update your policy. Examples:

- You move to a new city

- You buy a new car

- You add another driver

Not updating can cause problems if you need to make a claim.

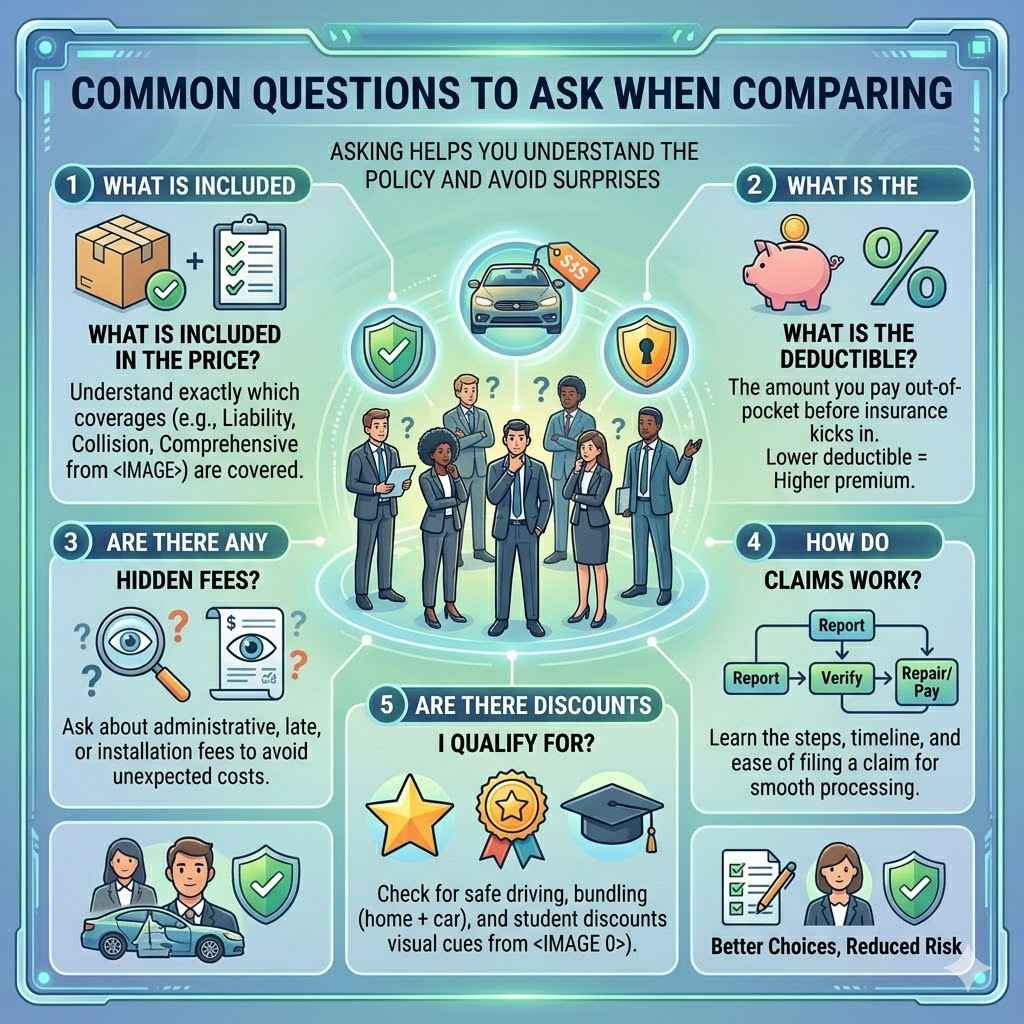

Common Questions To Ask When Comparing

When you compare, ask these questions:

- What is included in the price?

- What is the deductible?

- Are there any hidden fees?

- How do claims work?

- Are there discounts I qualify for?

Asking helps you understand the policy and avoid surprises.

Frequently Asked Questions

What Is The Best Way To Compare Car Insurance Prices?

The best way is to use online comparison tools and talk to an insurance agent. Start by knowing what coverage you need. Enter your details on several sites. Check coverage levels, deductibles, and discounts. Ask questions if anything is unclear.

Compare both price and service.

How Can I Make Sure I Am Comparing The Same Coverage?

Always check the policy details. Look at coverage types, limits, deductibles, and exclusions. If you are comparing liability coverage, make sure each quote covers the same amount. If you add collision or comprehensive, compare those too. Never compare just the price without looking at what’s included.

Why Do Car Insurance Prices Change So Much From One Company To Another?

Companies use different formulas to set prices. They look at your personal history, car details, location, and more. Some companies offer more discounts, while others focus on coverage. Prices also change based on their risk models and business costs.

What Should I Do If I Find A Much Cheaper Price?

Check why it’s cheaper. Look at the coverage, deductible, and company reputation. Sometimes low prices mean less protection or high fees. Make sure you understand what you are getting. If everything matches, and the company is reliable, it can be a good deal.

Can I Switch Car Insurance Anytime?

Yes, you can switch anytime, but check for cancellation fees or refund rules. It’s best to wait until your policy is ending to avoid extra costs. If you find a better deal, contact your current insurer and new insurer to make the change smoothly.

Comparing car insurance prices is not just about saving money. It’s about getting the right protection for you and your family. Take time to check details, ask questions, and review options. With careful comparison, you will find a policy that fits your needs and budget, and you’ll drive with peace of mind.