Cheapest Car Insurance Comparison Site UK (Updated Guide)

Finding the Cheapest Car Insurance Comparison Site UK (Updated Guide) can seem tricky at first. Many people wonder where to even start looking for good deals on car insurance. It feels like there are so many options!

But don’t worry, this guide will make it super simple. We will break it down step-by-step to help you find the best price without any fuss. Get ready to discover how easy it can be to save money on your car insurance.

Finding The Cheapest Car Insurance Comparison Site UK

This section helps you understand what to look for when searching for the cheapest car insurance deals in the UK. We will cover the main things that affect your car insurance price and how a comparison site can help you get the best quotes. It’s about making smart choices to save money.

We will guide you through the process so you can feel confident. Think of this as your friendly guide to getting great value on your insurance. It’s all about getting the most for your money.

How Comparison Sites Work

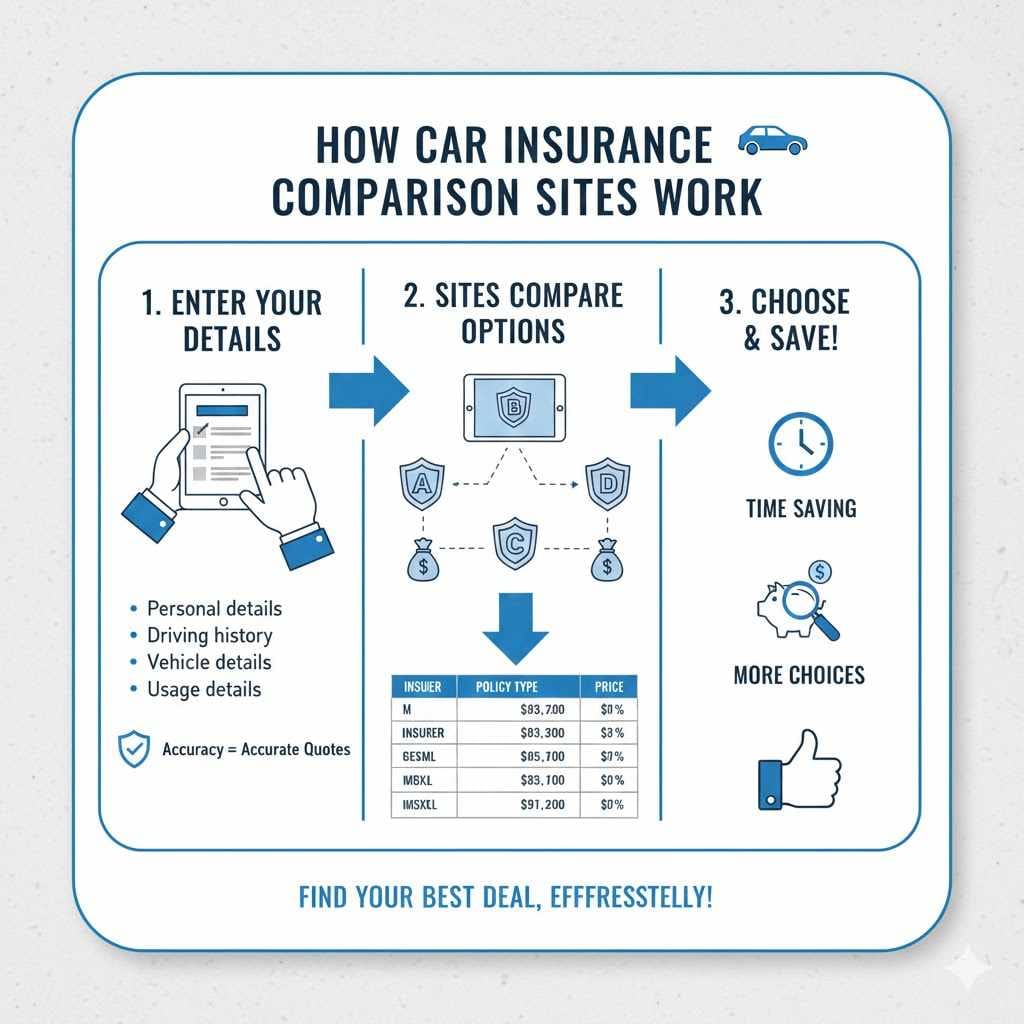

Car insurance comparison sites are online tools that let you get quotes from many different insurance companies all at once. You fill in your details just once, and the site shows you a list of prices. This saves you the time and effort of visiting each insurer’s website separately.

They work by partnering with various insurance providers. When you enter your information, they send it to these companies to get a quote. Then, they display all the results for you to compare easily.

This is a quick way to see who offers the cheapest deal for your specific needs. They aim to present a wide range of options.

What Information Is Needed

To get accurate quotes, you will need to provide some personal and vehicle information. This includes your date of birth, address, and driving history. You will also need details about your car, such as its make, model, age, and registration number.

Other factors like how many miles you drive each year and where you park your car overnight are also important. Insurers use this data to calculate your risk and set a price. The more precise you are, the more accurate your quotes will be.

Always double-check your details before submitting.

Here’s a list of common information requested:

- Personal details: Name, address, date of birth, occupation.

- Driving history: Driving licence number, claims history, any past convictions.

- Vehicle details: Make, model, year, registration number, estimated annual mileage, where it’s kept.

- Usage details: How the car is used (e.g., commuting, social use), who drives it.

Why Use A Comparison Site

Using a comparison site is one of the easiest ways to find the cheapest car insurance. It saves you a lot of time. Instead of visiting ten different insurance websites, you visit one.

You get many quotes quickly. This helps you see the full picture of what’s available. It can also lead to cheaper prices because it introduces competition among insurers.

They know you are comparing, so they try to offer their best deals. Many people find that comparison sites help them discover policies they didn’t know existed. It’s a very efficient way to shop around.

Here are some key benefits:

- Time saving: Get multiple quotes in minutes.

- Cost saving: Easily spot the cheapest options.

- Convenience: All quotes in one place.

- Awareness: Discover different insurers and policy types.

Factors Affecting Your Insurance Costs

Several things can influence how much you pay for car insurance. Insurers look at your personal details and your car. For example, your age is a big factor.

Younger drivers often pay more because they are seen as higher risk. Your driving record also matters. If you have had accidents or points on your licence, your premiums will likely be higher.

The type of car you drive is important too. Expensive cars or those that are easy to steal can cost more to insure. The amount of mileage you do and where you live also play a part.

Even the time of year you buy insurance can make a small difference.

Driver Demographics

Your personal characteristics significantly impact car insurance premiums. Age is a primary driver, with younger drivers typically facing higher costs due to their inexperience. Drivers in their early twenties might pay substantially more than someone in their fifties.

Similarly, the gender of the driver used to influence prices, though this is now less common due to regulations. Your occupation can also be a factor; some jobs are seen as higher risk than others. For instance, a journalist who travels extensively might be viewed differently than an office worker.

Your address is another key element. Living in an urban area with higher crime rates or accident statistics often leads to pricier insurance compared to a rural setting.

Vehicle Characteristics

The car you drive is a major determinant of your insurance cost. Cars are categorized into different insurance groups based on their repair costs, performance, and safety features. A small, economical car will generally be cheaper to insure than a high-performance sports car.

The car’s age also matters; older cars might be cheaper to insure if they are not worth a lot, but they might lack modern safety features. The engine size and power output are also considered. Cars with larger engines or turbochargers tend to be more expensive to insure.

The likelihood of theft is another factor; vehicles that are commonly targeted by thieves will have higher premiums.

Here are common vehicle factors:

- Make and model: Some cars are inherently more expensive to repair or more likely to be stolen.

- Engine size and power: Higher performance cars generally cost more to insure.

- Age of vehicle: Older cars might have fewer safety features, while very new cars can be more expensive to replace.

- Security features: Cars with advanced anti-theft systems might receive discounts.

Driving History And Claims Record

Your past driving behaviour is a strong indicator for insurance companies. A clean driving record, meaning no accidents or traffic violations, will usually result in lower premiums. Insurers often ask about your claims history over the past five years.

If you have made multiple claims, even if they were not your fault, this can increase your insurance cost. Points on your licence from speeding tickets or other offences are also a significant factor. Some insurers offer no-claims bonuses, where you get a discount for every year you don’t make a claim.

This can substantially reduce your premium over time. It’s important to be honest about your claims history.

Annual Mileage And Where You Park

The number of miles you drive each year has a direct impact on your insurance premium. If you drive very little, you are less likely to be involved in an accident, so your premium will be lower. When you use a comparison site, you will be asked for your estimated annual mileage.

Being accurate is important; if you underestimate and then drive more, your policy might not cover you fully. Where you park your car overnight also matters. Cars parked on a driveway or in a locked garage are generally considered safer than those parked on the street.

Street parking can increase the risk of theft or damage, leading to higher insurance costs.

Comparing Different Types Of Cover

When you look for car insurance, you will see different levels of cover. The most common are Third Party, Third Party Fire and Theft, and Fully Comprehensive. Each offers a different amount of protection.

It’s important to understand what each one means for you and your wallet. Choosing the right level of cover balances cost with protection. Many people think fully comprehensive is always the most expensive, but this isn’t always the case.

Sometimes, fully comprehensive can actually be cheaper than other types for certain drivers.

Third Party Insurance

Third Party insurance is the most basic level of car insurance required by law in the UK. It covers damage or injury you might cause to other people, their vehicles, or their property. However, it does not cover any damage to your own car.

If you have an accident that is your fault, your car won’t be repaired by your insurance. This type of cover is usually the cheapest. It’s important to remember that this cover only protects others, not you or your vehicle.

Third Party Fire And Theft

This level of cover is a step up from Third Party insurance. It includes everything Third Party cover does, plus it covers your car if it is stolen or damaged by fire. It still doesn’t cover damage to your car if you have an accident that is your fault.

So, if you crash your car, repairs to your own vehicle won’t be paid for. However, if your car is stolen or catches fire, your insurer will pay out to replace or repair it. This option offers a bit more protection for your own vehicle compared to basic Third Party.

Fully Comprehensive Insurance

Fully Comprehensive insurance provides the highest level of protection. It covers damage to other people’s property and injuries, as well as damage to your own car, even if the accident was your fault. It also usually includes cover for theft and fire.

Despite its name, Fully Comprehensive cover is not always the most expensive option. For some drivers, especially younger ones, it can sometimes be cheaper than Third Party or Third Party Fire and Theft. This is because insurers sometimes see these drivers as higher risk and a fully comprehensive policy might offer them better value.

Here is a comparison table for cover types:

| Cover Type | Covers Others’ Property/Injury | Covers Your Car (Theft/Fire) | Covers Your Car (Accident Fault) | Typical Cost |

|---|---|---|---|---|

| Third Party | Yes | No | No | Lowest |

| Third Party Fire & Theft | Yes | Yes | No | Medium |

| Fully Comprehensive | Yes | Yes | Yes | Can be Lowest/Medium |

Tips For Getting The Cheapest Car Insurance

Saving money on car insurance is possible with a few smart strategies. It’s not just about finding the cheapest quote on a comparison site. You can also make adjustments to your policy or how you pay for it.

Think about your driving habits and your car. Small changes can lead to noticeable savings. We will explore practical tips that can help you reduce your insurance costs.

These are simple steps you can take to get the best deal. It’s about being informed and making the right choices for your situation.

Adjusting Your Policy Details

Sometimes, small changes to your policy details can lower your premium. Consider increasing your excess. The excess is the amount you pay towards a claim.

A higher excess usually means a lower premium. However, make sure you can afford to pay the excess if you need to make a claim. Review your annual mileage and be realistic.

If you drive less than you estimated, inform your insurer. Also, think about who is listed as the main driver. Adding a more experienced driver with a clean record, even if they don’t drive the car often, might reduce your premium.

However, be honest about who drives the car most.

Paying Annually Instead Of Monthly

One of the most effective ways to save money is to pay for your car insurance in one go annually, rather than spreading the cost monthly. Most insurance companies charge interest on monthly payments. This means that by the end of the year, you will have paid more than if you had paid the full amount upfront.

Paying annually can save you a significant percentage of your total premium. If you don’t have the full amount readily available, consider saving up for it or looking into 0% interest credit cards if you can manage the repayment. The savings can be quite substantial.

Increasing Your Voluntary Excess

Increasing the amount of voluntary excess you are willing to pay can directly lower your car insurance premium. The voluntary excess is an amount you agree to pay towards any claim you make. This is in addition to the compulsory excess, which is set by the insurer and is often lower.

For example, if your voluntary excess is £200, and you have an accident causing £1,000 worth of damage, you would pay £200, and the insurer would pay £800. If you increase your voluntary excess to £500, your premium would likely decrease, but you would then pay £500 towards that claim. It’s a trade-off that requires careful consideration of your financial situation.

Improving Your Car’s Security

Making your car more secure can lead to lower insurance premiums. Insurers often offer discounts for vehicles fitted with specific security devices. These can include factory-fitted alarms, immobilisers, and tracking systems.

If you park your car in a secure location, such as a locked garage or a private driveway, this also reduces risk and can lower your costs. Some insurers may even offer a discount if you belong to a neighbourhood watch scheme. Always inform your insurer about any security improvements you make, as they may not be aware of them otherwise.

These measures show insurers that you are taking proactive steps to protect your vehicle.

Consider A Telematics Policy (Black Box)

Telematics insurance, often referred to as “black box” insurance, uses a small device installed in your car to monitor your driving habits. This device records data such as your speed, acceleration, braking, and time of day you drive. Safer drivers, who adhere to speed limits and drive smoothly, often receive significant discounts on their premiums.

This type of policy is particularly beneficial for young or newly qualified drivers who are looking to reduce their insurance costs. It encourages safer driving by directly linking good behaviour to lower prices. However, be aware that poor driving could lead to higher premiums or even cancellation of the policy.

Here’s a scenario for telematics:

- A new driver, aged 19, gets a quote for standard comprehensive insurance that is £2,500 per year.

- They then explore telematics insurance and get a quote for £1,800 per year, with the potential to earn further discounts based on their driving.

- After six months of driving safely, their insurer offers a £300 refund, bringing the annual cost down to £1,500.

Understanding Policy Terms And Conditions

It is vital to read and understand the terms and conditions of any car insurance policy before you buy it. This document outlines what is covered and, just as importantly, what is not covered. Misunderstanding these details can lead to disappointment or financial loss if you need to make a claim.

We will break down some key areas to pay attention to. Knowing these terms helps you make an informed decision and avoid unexpected issues. It’s all part of ensuring you have the right protection for your needs.

Policy Exclusions

Every insurance policy has exclusions, which are specific situations or circumstances where the insurer will not pay out. Common exclusions include damage caused while driving under the influence of alcohol or drugs, or if the driver is not legally licensed. Driving in a dangerous manner or participating in illegal racing are also typical exclusions.

Wear and tear on your vehicle, mechanical breakdown, and damage from faulty workmanship are usually not covered. It’s crucial to know these limitations so you don’t rely on your insurance for things it won’t cover. Always check the policy document for a full list of exclusions.

Common Exclusions To Watch For

When reviewing your policy, look out for exclusions related to:

- Driving without a valid licence or insurance.

- Driving while intoxicated or under the influence of drugs.

- Damage resulting from illegal street racing or speeding.

- Mechanical failures, breakdowns, or general wear and tear.

- Damage from natural disasters like floods or earthquakes (unless specifically included).

- Theft of personal belongings from the car (this is usually covered by home insurance).

Excess And Deductibles Explained

The term ‘excess’ and ‘deductible’ are often used interchangeably in insurance. In the UK, ‘excess’ is the more common term. It refers to the amount of money you agree to pay towards a claim.

There are two main types: compulsory excess and voluntary excess. The compulsory excess is set by the insurer and is based on factors like the car and driver’s age. The voluntary excess is an amount you choose to add.

You can usually increase your voluntary excess to lower your premium, but remember you will have to pay this amount if you make a claim. For example, if a repair costs £1,000 and your total excess is £400, you will pay £400 and the insurer will pay £600.

No-Claims Bonus

A no-claims bonus (NCB), also known as a no-claims discount, is a reward for drivers who have not made an insurance claim. For each year you drive without making a claim, you build up a no-claims bonus. This can significantly reduce the cost of your car insurance.

Most insurers allow you to build up a maximum of around 15 years of no-claims bonus. Some insurers offer protected no-claims bonuses, which means you can make a certain number of claims over a period of years without losing your discount. This protection usually comes at an extra cost.

It’s vital to protect your NCB by driving safely and avoiding unnecessary claims.

Protecting Your No-Claims Bonus

You can protect your no-claims bonus in a couple of ways:

- Protected No-Claims Bonus: For an additional fee, your insurer may allow you to keep your NCB even if you make a claim. This usually means you can have one or two claims within a set period (e.g., three years) without affecting your discount.

- Guaranteed No-Claims Bonus: Some policies offer a guaranteed NCB, meaning your discount will not be affected by claims. This is less common and often more expensive.

It’s important to understand the terms of any NCB protection. For instance, it might only apply if the claim is not your fault. Always check the policy details carefully.

Make And Model Specifics

The make and model of your car have a substantial impact on its insurance cost. This is due to several factors, including the car’s value, repair costs, performance, and its popularity with thieves. High-performance sports cars, for example, will almost always be more expensive to insure than a small, practical family car.

Luxury vehicles often have higher repair bills, increasing premiums. Cars that are frequently targeted by car thieves will also carry higher insurance premiums because the risk of a claim is greater. Insurers use a system of ‘insurance groups’ to categorise vehicles, with higher group numbers indicating higher risk and therefore higher insurance costs.

You can often find out the insurance group for a specific car model online.

Here are some examples of car types and their typical insurance group impacts:

| Car Type | Typical Insurance Group | Reason for Group |

|---|---|---|

| Small City Car (e.g., Fiat 500) | Low (e.g., 1-10) | Low cost to repair, economical, less theft risk. |

| Family Hatchback (e.g., Ford Focus) | Medium (e.g., 11-20) | Balanced performance, repair costs, and safety. |

| Performance Car (e.g., BMW M3) | High (e.g., 30+) | High performance, expensive parts, higher theft risk. |

| Luxury Saloon (e.g., Mercedes-Benz S-Class) | High (e.g., 25+) | Expensive to repair, high value. |

Frequently Asked Questions

Question: How can I find the cheapest car insurance online

Answer: Use reputable car insurance comparison websites. These sites allow you to compare quotes from many different insurers at once by filling in your details just once. Always compare a few different sites to get the widest range of options and prices.

Question: Is fully comprehensive insurance always the most expensive

Answer: No, not always. For some drivers, particularly younger or newer drivers, fully comprehensive cover can sometimes be cheaper than third-party options because insurers assess risk differently.

Question: What is a no-claims bonus and how does it work

Answer: A no-claims bonus is a discount you receive for each year you go without making an insurance claim. The longer you have a no-claims bonus, the lower your insurance premium is likely to be.

Question: Should I be honest about my annual mileage

Answer: Yes, absolutely. It is crucial to provide an accurate estimate of your annual mileage. Underestimating your mileage can lead to your insurance being invalid if you have an accident and the insurer discovers you exceeded the declared amount.

Question: What is the difference between voluntary and compulsory excess

Answer: Compulsory excess is set by the insurer based on your risk factors. Voluntary excess is an amount you choose to pay towards a claim, and increasing this can lower your premium, but you must be able to afford to pay it if a claim occurs.

Summary

Finding the cheapest car insurance comparison site UK involves understanding your needs and what insurers look for. Use comparison sites to gather multiple quotes and explore different cover levels. Always check policy details, understand exclusions, and consider ways to reduce your premium like paying annually or increasing excess.

Being truthful about your driving and car helps secure the best deal.