How to Compare Car Insurance Policies Like a Pro

It can be tough to figure out car insurance. Many people feel lost when they first look at policies. There’s a lot of jargon and different options.

But don’t worry! This guide will show you How to Compare Car Insurance Policies Like a Pro. We’ll break it down into simple steps.

You’ll learn what to look for and how to get the best coverage for your needs.

Understanding Car Insurance Basics

This section helps you get a handle on what car insurance actually is. We’ll cover the main types of coverage you’ll see. Knowing these terms is the first step to making smart choices. It’s like learning the rules of a game before you play. We’ll make sure you know what each part means so you can pick what’s right for you.

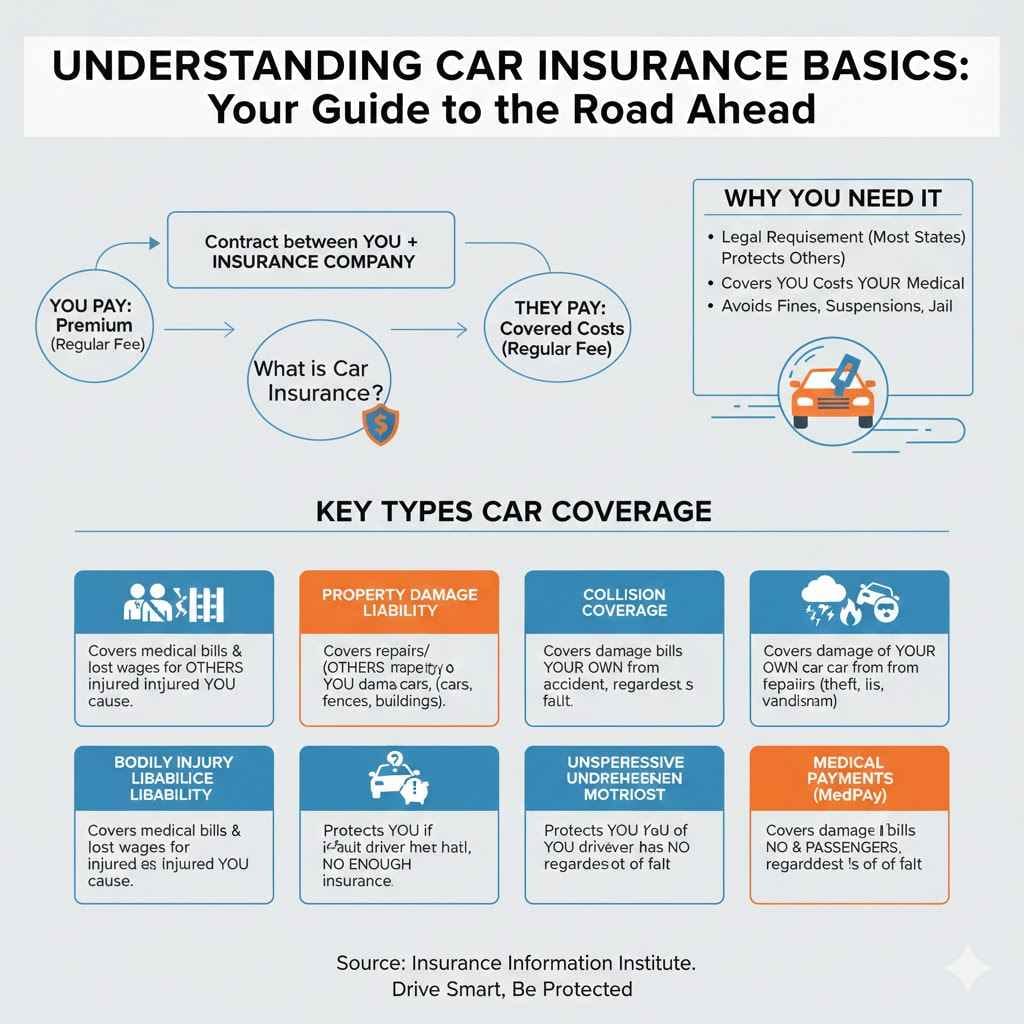

What Is Car Insurance

Car insurance is a contract between you and an insurance company. You pay a regular amount, called a premium. In return, the company agrees to pay for certain costs if you have an accident or your car is damaged. This protects you from huge bills if something bad happens. It’s a safety net for your finances.

Why You Need Car Insurance

Driving without insurance can lead to serious trouble. Most places require drivers to have at least a minimum level of coverage. This is to protect other people if you cause an accident. It also covers costs like car repairs or medical bills. Without it, you could face fines, have your license suspended, or even go to jail.

Key Types of Coverage

There are several common types of car insurance coverage. Understanding these is key to comparing policies effectively. Each one covers something different.

Bodily Injury Liability Coverage

This pays for medical bills and lost wages for people injured in an accident you cause. It’s designed to help cover their recovery costs. Your policy will have a limit for how much it will pay per person and per accident.

Property Damage Liability Coverage

This covers costs to repair or replace other people’s property that you damage in an accident. This usually means their cars, but it can also include fences, buildings, or other property. Like bodily injury, there’s a limit to how much your policy covers.

Collision Coverage

This helps pay to repair or

Comprehensive Coverage

This covers damage to your car that isn’t from a collision. Think theft, vandalism, fire, or natural disasters like hail. It’s also usually optional but recommended for newer or valuable vehicles.

Uninsured/Underinsured Motorist Coverage

This protects you if you’re in an accident with a driver who has no insurance or not enough insurance to cover your damages. It can cover your medical bills and car repairs.

Medical Payments Coverage (MedPay)

This covers medical expenses for you and your passengers, no matter who is at fault for the accident. It can help pay for things like doctor visits and hospital stays.

How to Compare Car Insurance Policies Like a Pro

Now that you know the basics, let’s talk about how to actually compare policies. This is where you become a smart shopper. It’s not just about the price. It’s about finding the best value and the right protection for your situation. We’ll walk through the steps to do this like a pro.

Gathering Your Information

Before you start looking at policies, get your facts together. The more accurate information you have, the better your quotes will be. Insurance companies need certain details to give you a price. Having this ready saves time and ensures you get accurate quotes.

- Vehicle Information

You’ll need details about your car. This includes the make, model, year, and Vehicle Identification Number (VIN). The VIN is like a fingerprint for your car. It helps insurers identify the exact features and safety equipment. - Driver Information

This includes your name, address, date of birth, and driver’s license number. Insurers also ask about your driving history. This means any accidents, tickets, or claims you’ve had. - Current Insurance Details

If you have insurance now, have your current policy handy. This includes your coverage levels and limits. Some insurers might ask for your policy number or declaration page.

Getting Multiple Quotes

This is a super important step. Never just go with the first quote you get. Prices can vary a lot between different companies. You need to shop around to find the best deal. Aim to get quotes from at least three to five different insurers.

Online Comparison Tools

Many websites allow you to compare quotes from multiple companies at once. You enter your information one time, and they show you different offers. These tools can be a quick way to see a broad range of prices. They are great for a starting point.

Directly From Insurers

You can also get quotes directly from insurance company websites. This often gives you access to more specific discounts or bundles. It’s also a good way to build a relationship with an insurer if you find one you like.

Through an Insurance Agent

Independent insurance agents can get quotes from many different companies for you. They can also offer expert advice. They work for you, not a single insurance company. This can be helpful if you want personalized guidance.

Understanding Policy Costs

The price you pay for insurance is your premium. This can be paid monthly, semi-annually, or annually. Many factors affect your premium. Understanding these helps you see why one policy might be cheaper than another.

Premium Factors

Insurers look at many things to set your premium. This includes your driving record, where you live, the type of car you drive, your credit score (in most states), and how much coverage you choose. A history of speeding tickets or accidents will usually increase your rates. Living in an area with high theft rates can also make insurance more expensive.

Deductibles Explained

A deductible is the amount you pay out-of-pocket before your insurance company starts paying. For example, if you have a $500 deductible and a $3,000 repair bill, you pay the first $500, and the insurer pays the remaining $2,500. Choosing a higher deductible often means a lower premium. However, make sure you can afford to pay the deductible if you need to file a claim.

Discounts Available

Most insurance companies offer discounts. Asking about these can significantly lower your premium. Common discounts include:

- Multi-policy discount

If you bundle your car insurance with your home or renters insurance from the same company. - Safe driver discount

For having a clean driving record with no accidents or tickets for a certain period. - Good student discount

For young drivers who maintain good grades. - Low mileage discount

If you don’t drive many miles each year. - Vehicle safety features discount

For cars with anti-lock brakes, airbags, or anti-theft devices.

Evaluating Coverage Levels and Limits

Comparing prices is important, but so is making sure you have enough coverage. A cheap policy with inadequate protection can cost you a lot more in the long run. You need to balance cost with security.

Assessing Your Coverage Needs

Your needs depend on your personal situation. Consider your car’s value, your financial situation, and your risk tolerance. If you have a new, expensive car, you’ll likely want collision and comprehensive coverage. If you have a lot of savings, you might be comfortable with higher deductibles.

What is Enough Coverage

There’s no single answer for everyone. State minimums are usually very low and may not be enough to cover a serious accident. Experts often recommend carrying bodily injury liability coverage of at least $100,000 per person and $300,000 per accident. For property damage, $50,000 is often suggested. Consider your assets. If you own a home or have significant savings, you need enough liability coverage to protect them.

Comparing Policy Limits

Policy limits are the maximum amounts an insurance company will pay for a covered loss. You’ll see these listed as numbers, like 100/300/50. This means $100,000 for bodily injury per person, $300,000 for bodily injury per accident, and $50,000 for property damage per accident.

Example Scenario Comparison

Let’s say you’re comparing two policies:

Policy A:

Bodily Injury Liability: $50,000/$100,000

Property Damage Liability: $25,000

Collision Deductible: $1,000

Comprehensive Deductible: $500

Premium: $1,200 per year

Policy B:

Bodily Injury Liability: $100,000/$300,000

Property Damage Liability: $50,000

Collision Deductible: $500

Comprehensive Deductible: $250

Premium: $1,600 per year

If you cause an accident resulting in $150,000 in medical bills for one person and $60,000 in car damage, Policy A would leave you responsible for $100,000 of the medical bills ($150,000 – $50,000) and $35,000 of the car damage ($60,000 – $25,000). Policy B would cover all the medical bills and $10,000 of the car damage. Policy B costs more in premiums, but it offers much better protection against a large financial loss.

Understanding Deductible Impacts

Choosing your deductible wisely is crucial. A higher deductible lowers your premium. However, if you have an accident, you’ll have to pay more out-of-pocket.

Scenario: A $4,000 car repair.

Option 1: $500 Deductible

You pay: $500

Insurer pays: $3,500

Premium: Higher

Option 2: $1,000 Deductible

You pay: $1,000

Insurer pays: $3,000

Premium: Lower

Consider your savings. If you have $2,000 in savings, you can afford either deductible. If you only have $700 saved, a $1,000 deductible might be risky.

Reading the Fine Print

Once you’ve narrowed down your choices, take time to read the policy documents carefully. Don’t just look at the summary. The details matter and can affect what is covered. This is where you can find important exclusions or specific conditions.

Key Policy Exclusions

Every insurance policy has exclusions. These are specific situations or damages that the insurance company will not cover. It’s vital to know these to avoid surprises.

- Intentional Acts

Damage caused intentionally by you is never covered. - Racing and Speed Contests

Participating in illegal street races or organized speed contests voids coverage. - Wear and Tear

Normal aging and deterioration of your vehicle are not covered. - Certain Modifications

Some aftermarket modifications may not be covered or could void your policy.

Understanding Policy Limitations

Limitations are different from exclusions. They often refer to the caps on coverage or specific conditions that must be met. For example, a policy might have a limit on rental car reimbursement per day or per incident.

When to Consult an Agent

If you find any part of the policy confusing, don’t hesitate to ask questions. An insurance agent can explain complex terms or clauses. They can help you understand what the policy truly means for you. It’s better to ask now than to find out later you misunderstood something important.

How to Compare Car Insurance Policies Like a Pro: Real-World Statistics and Examples

To further illustrate why comparing policies is so important, let’s look at some data and common situations. The numbers show how much you can save and the potential pitfalls of not shopping around.

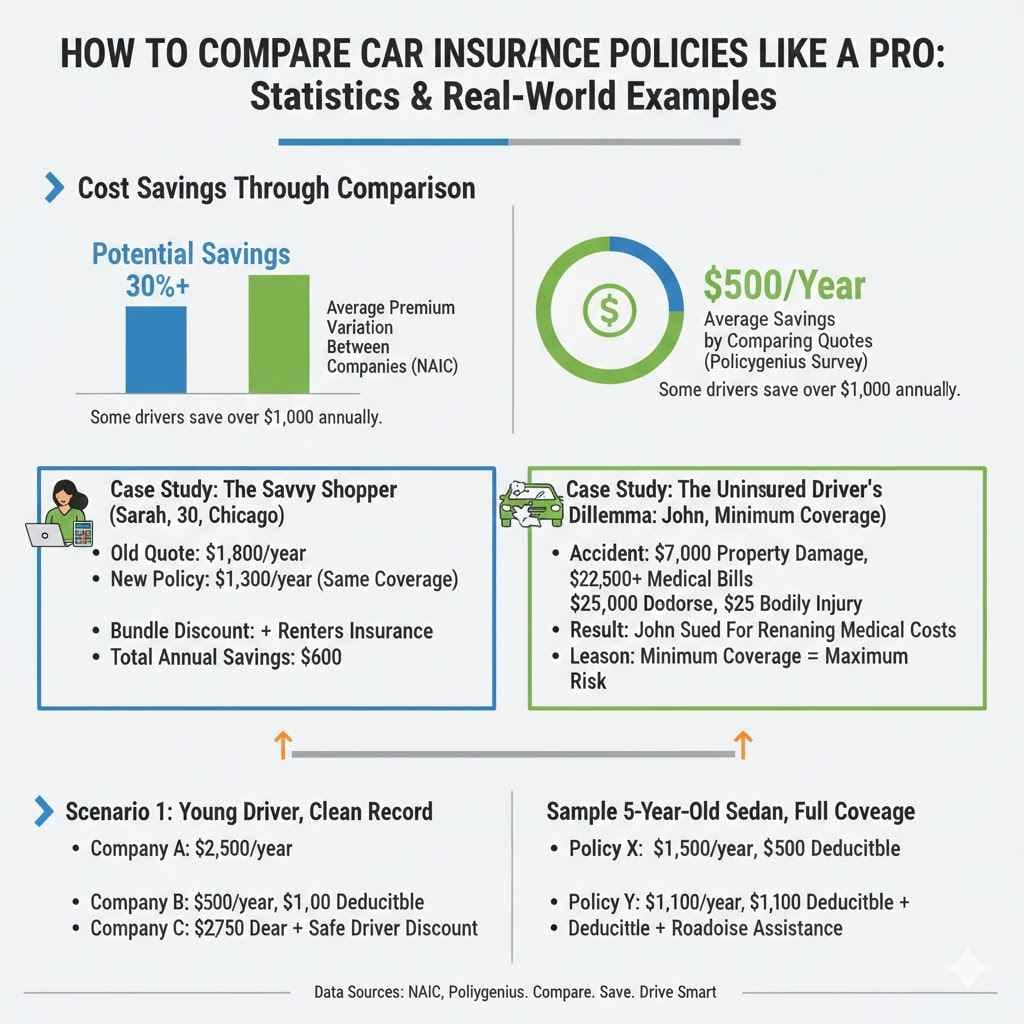

Cost Savings Through Comparison

Studies consistently show that drivers can save money by comparing quotes. According to the National Association of Insurance Commissioners (NAIC), average car insurance premiums can vary by more than 30% between different companies for the same coverage.

A 2023 survey by Policygenius found that drivers could save an average of $500 per year by comparing quotes. Some drivers even reported saving over $1,000 annually. This highlights the significant financial benefit of actively shopping for insurance.

Case Study: The Savvy Shopper

Sarah, a 30-year-old driver from Chicago, needed to renew her car insurance. Her current insurer quoted her $1,800 for a year of full coverage. Instead of accepting this, Sarah spent an afternoon comparing quotes online and speaking with an independent agent.

She found a policy with similar coverage limits and deductibles from a different company for $1,300 per year. She also learned about a discount for bundling her auto and renters insurance, bringing her total savings to $600 for the year. Sarah’s proactive approach saved her a substantial amount of money without sacrificing coverage.

Case Study: The Uninsured Driver’s Dilemma

John was involved in a minor fender-bender. He was only carrying the state-required minimum liability coverage. The other driver’s car had $7,000 in damages, and their neck was injured, requiring medical treatment. John’s liability policy only covered $3,000 for property damage and $25,000 for bodily injury per person.

John’s insurance paid out $3,000 for the car. However, the medical bills exceeded $25,000. John was personally sued for the remaining medical expenses. Because he didn’t have enough bodily injury liability coverage, John ended up having to pay thousands of dollars out of his own savings to cover the medical costs. This shows the risk of relying on minimum coverage.

Sample Scenarios for Comparison

Here are two common scenarios illustrating why comparing is key:

1.

You are a young driver with a clean record looking for insurance.

Company A offers a policy for $2,500 per year with a $1,000 deductible.

Company B offers a policy for $2,000 per year with a $500 deductible.

Company C offers a policy for $2,200 per year with a $750 deductible and a safe driver discount.

Comparing these options helps you see which offers the best balance of cost and deductible for your budget and risk comfort level.

2.

You own a 5-year-old sedan and are comparing comprehensive and collision coverage.

Policy X has a $500 deductible for both comprehensive and collision, costing $1,500 annually.

Policy Y has a $1,000 deductible for both, costing $1,100 annually.

Policy Z has a $750 deductible for both and includes roadside assistance, costing $1,300 annually.

In this case, you weigh the cost savings of a higher deductible against the potential out-of-pocket expense in an accident and the value of added features like roadside assistance.

Frequently Asked Questions

Question: What is the best way to get car insurance quotes

Answer: The best way is to get quotes from multiple sources. Use online comparison tools, visit individual insurance company websites, and consider talking to an independent insurance agent.

Question: How often should I compare car insurance policies

Answer: You should compare policies at least once a year, or whenever you experience a major life change like moving, buying a new car, or having a change in your driving record.

Question: Can I get cheaper car insurance with a lower deductible

Answer: Typically, a higher deductible will result in a lower premium. However, you must be able to afford to pay the deductible amount if you need to file a claim.

Question: What if my car is totaled in an accident

Answer: If your car is totaled, your collision coverage will pay you the actual cash value of your car, minus your deductible. If you owe more on the car than it’s worth, gap insurance can help cover the difference.

Question: Are all car insurance policies the same

Answer: No, car insurance policies can vary greatly in coverage limits, deductibles, exclusions, and premium costs. It is important to compare them carefully.

Summary

Comparing car insurance policies requires looking beyond just the price. Understanding coverage types, limits, deductibles, and discounts helps you find the best value. Always get multiple quotes and read the policy details. This ensures you have the right protection for your needs and budget.