How to Compare Car Insurance Online: Save Big With Smart Choices

Comparing car insurance online is more than just finding the lowest price. With so many insurance companies and plans, it’s easy to feel lost. But if you know what matters, you can make a smart choice and save money. Whether you are buying your first policy or looking to switch providers, understanding how to compare car insurance online can help you protect your car, your wallet, and your peace of mind.

Many people click on the first price they see, but this often leads to regrets later. Car insurance is about more than cost—it’s about the right coverage, service, and support when you need it most. In this guide, you’ll discover how to compare car insurance online step by step, learn what factors truly matter, and find practical advice for making the best choice.

We’ll cover how to gather quotes, what to check in each policy, and tips that even experienced drivers sometimes forget.

Why Compare Car Insurance Online?

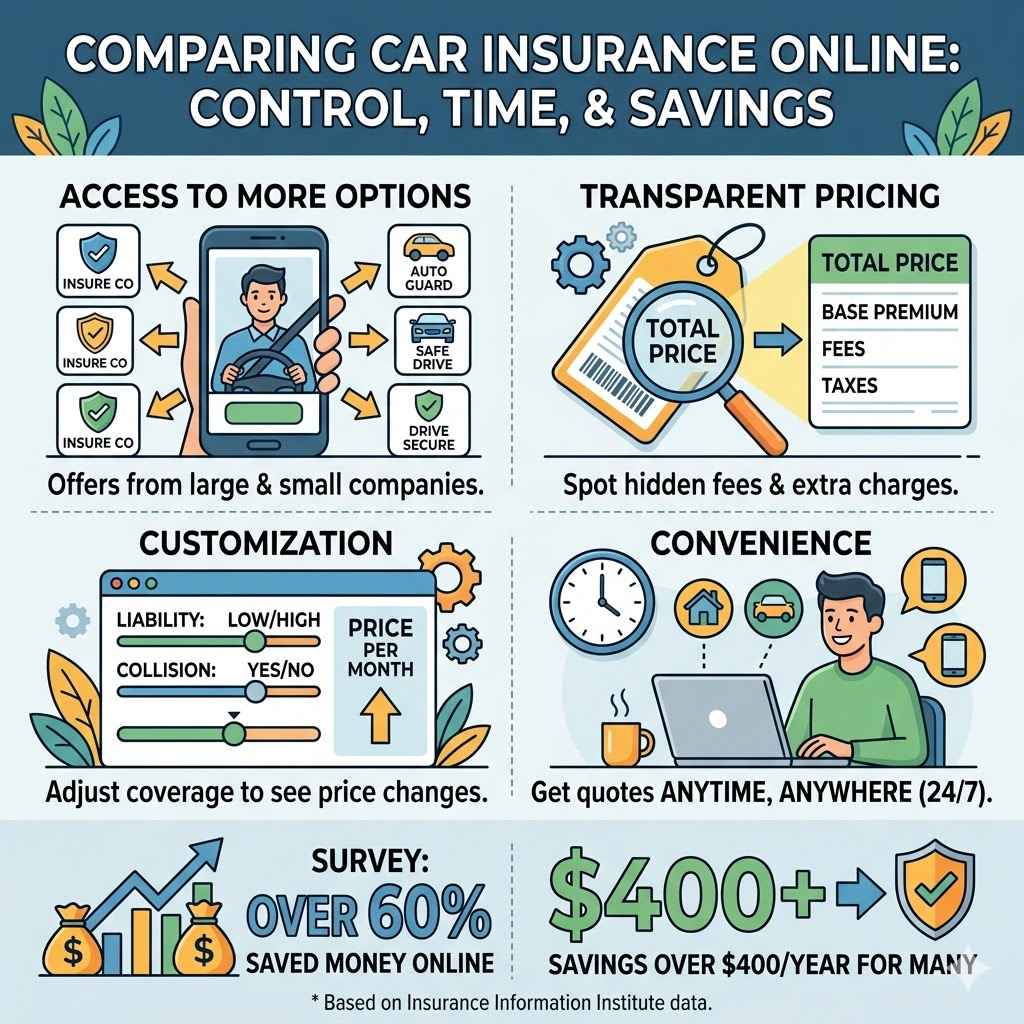

Comparing car insurance online gives you control and saves time. You can check offers from many companies without calling each one. Most insurance websites and comparison tools are free, fast, and easy to use.

Key benefits include:

- Access to more options: You see offers from big brands and smaller companies.

- Transparent pricing: You can spot hidden fees or extra charges.

- Customization: You can adjust coverage and see how it changes the price.

- Convenience: Get quotes anytime, anywhere.

A recent survey by the Insurance Information Institute found that more than 60% of drivers who compared policies online saved money, with many saving over $400 per year.

What Information You Need Before Comparing

Before you start, gather important details. Having everything ready makes the process faster and ensures you get accurate quotes.

- Personal information: Your name, address, date of birth, and driver’s license number.

- Car details: Make, model, year, Vehicle Identification Number (VIN), and mileage.

- Driving history: Past accidents, claims, and any tickets.

- Current insurance: Policy details and coverage limits.

- Desired coverage: What types and amounts of coverage you want.

Pro tip: Some comparison sites let you save your details for future use, making updates easy when you want to re-compare next year.

Key Factors That Affect Car Insurance Quotes

Understanding what impacts your quote helps you compare fairly. Here are the main factors:

- Age and driving experience: Young or new drivers usually pay more.

- Location: Urban areas often have higher rates due to more accidents and thefts.

- Car type: Expensive or sporty cars cost more to insure.

- Driving record: Tickets and accidents raise your price.

- Annual mileage: More miles means higher risk.

- Coverage type and limits: More coverage costs more, but gives better protection.

- Credit score: In many places, a better score means a lower price.

Different insurers weigh these factors differently. One company might be cheaper for young drivers, while another is better for experienced ones.

How To Compare Car Insurance Quotes Online

Let’s break down the process into simple steps:

1. Choose Reliable Comparison Sites

Start with well-known insurance comparison websites. These sites collect quotes from many insurers and present them side by side.

Examples of reputable sites:

- NerdWallet

- The Zebra

- Compare.com

Always double-check that the site is secure (look for https:// in the address) and read reviews before entering your information.

2. Enter Your Information Carefully

Accuracy is key. Small errors can change your quote or cause problems if you need to file a claim later.

- Use the exact spelling from your driver’s license.

- Enter your car details from the registration or insurance card.

- Be honest about accidents or claims.

3. Adjust Coverage Options

Most comparison tools let you change coverage limits and deductibles. Try different combinations to see how they affect your price.

For example, increasing your deductible from $500 to $1,000 usually lowers your premium, but you’ll pay more if you have an accident.

4. Review And Compare Results

You’ll see a list of offers with prices and basic coverage details. Don’t just pick the cheapest one. Look closely at what’s included.

Here’s a sample of what you might see:

| Company | Annual Premium | Liability Coverage | Comprehensive/Collision | Deductible |

|---|---|---|---|---|

| ABC Insurance | $950 | $100,000/$300,000 | Yes/Yes | $500 |

| XYZ Mutual | $1,100 | $50,000/$100,000 | Yes/No | $1,000 |

| SafeAuto | $980 | $100,000/$300,000 | Yes/Yes | $1,000 |

Notice that the lowest price may not offer the best coverage. Always match the coverage and deductible when comparing.

5. Dig Into Policy Details

Click through to see more about each offer. Look for:

- Coverage types included (liability, comprehensive, collision, uninsured motorist, etc.)

- Policy limits

- Deductibles

- Optional add-ons (roadside assistance, rental car, etc.)

- Discounts applied

Example: Two policies may cost the same, but one includes free roadside help and accident forgiveness, while the other does not.

6. Check Company Ratings

Before buying, check the insurer’s reputation. Financial strength and customer service matter when you need to file a claim.

Look for:

- AM Best or Moody’s ratings for financial stability

- J.D. Power or Consumer Reports for customer satisfaction scores

- Online reviews from real customers

A company with a slightly higher price but a strong reputation can be a safer bet.

7. Contact Insurers Directly (if Needed)

If you have questions or special needs (like insuring a classic car or needing business use coverage), call the company directly. Some smaller insurers might not appear on comparison sites.

Types Of Coverage To Compare

Understanding the main coverage types makes your comparison more meaningful.

Liability

Pays for damage and injuries you cause to others. Required in most states.

Collision

Covers your car if you hit another vehicle or object.

Comprehensive

Protects against theft, vandalism, fire, and weather events.

Uninsured/underinsured Motorist

Covers you if the other driver has no insurance or not enough.

Medical Payments/personal Injury Protection

Pays for medical bills after an accident.

Extras

Look for rental car coverage, roadside assistance, and gap insurance (for new cars).

Practical tip: Not all policies include extras by default. Make sure you know what you’re getting.

Common Mistakes When Comparing Car Insurance Online

Many drivers make errors that cost them money or leave them under-protected.

- Focusing only on price: Cheap policies often have low coverage or high deductibles.

- Not matching coverages: Comparing a basic policy with a full-coverage policy is not fair.

- Ignoring company reputation: A low price is useless if the company is hard to deal with after a claim.

- Missing discounts: Many insurers offer savings for bundling policies, safe driving, or good grades.

- Giving incomplete info: Wrong details can lead to canceled policies or denied claims.

- Overlooking exclusions: Some policies exclude drivers under 25, rideshare use, or certain repairs.

Using Comparison Tools Vs. Direct Quotes

While comparison tools are helpful, sometimes it’s smart to get a quote straight from the insurer’s website. Some companies offer better prices or special discounts for buying direct.

Here’s a look at both options:

| Method | Pros | Cons |

|---|---|---|

| Comparison Sites | Fast, see many offers at once, easy to adjust coverage | Some insurers not included, details may be basic |

| Direct Quotes | May find lower price, get all available discounts, ask questions | Slower, more work to compare multiple companies |

Many smart shoppers use both methods to make sure they don’t miss a better deal.

Discounts You Should Ask About

Car insurance companies offer many types of discounts. Some are automatic, but others you must request.

- Multi-policy: Bundle car and home insurance for a discount.

- Safe driver: No accidents or tickets in recent years.

- Good student: Young drivers with good grades.

- Low mileage: Drive less than average per year.

- Anti-theft device: Car has alarm or tracking system.

- Pay-in-full: Pay your premium all at once.

- Paperless billing: Receive documents electronically.

Always ask what discounts are available before buying.

Comparing Service And Claims Experience

Price is important, but service matters most when you need help. Check each company’s claims process and customer support.

- How easy is it to file a claim?

- Is there 24/7 support?

- Are repairs handled quickly?

- Does the company have a good reputation for paying claims?

Some companies offer mobile apps that let you track claims, upload photos, or get roadside help instantly.

Reading The Fine Print: Exclusions And Conditions

Insurance policies often have exclusions—things they do not cover. Read these carefully before buying.

Examples of common exclusions:

- Using your car for Uber/Lyft without special coverage

- Racing or illegal use

- Some aftermarket parts

- Flood or earthquake damage (unless included)

Ask for a summary of exclusions if you are unsure.

How To Switch Policies Safely

If you find a better deal, switching is usually simple. But avoid gaps in coverage.

- Confirm your new policy start date.

- Cancel your old policy only after the new one is active.

- Ask for a cancellation confirmation in writing.

- If you paid ahead, request a refund for unused time.

Non-obvious insight: Some states charge a fee for canceling early, so check your current policy.

When And How Often To Compare

You should compare car insurance at least once per year, or whenever your situation changes:

- New car or driver

- Move to a new area

- Accident or claim

- Big life event (marriage, divorce)

Rates can change even if nothing else does, so regular comparison keeps your price fair.

Special Cases: Comparing For Young Drivers, Seniors, And High-risk Drivers

Young Drivers

Rates are highest for drivers under 25. Look for companies with good student or driver training discounts. Adding a young driver to a parent’s policy is often cheaper.

Seniors

Some insurers give discounts to drivers over 55 who complete safe driving courses. Compare senior-friendly providers for the best rates.

High-risk Drivers

If you have a poor driving record, not all companies will insure you. Focus on insurers that specialize in high-risk coverage, but compare carefully—prices and coverage can vary a lot.

Privacy And Security When Comparing Online

When you enter personal data online, check for:

- A padlock symbol in your browser (means the site is secure)

- Privacy policy details

- No requests for unnecessary details (like full Social Security Number)

Never share payment details before you are ready to buy.

Non-obvious Tips For A Smarter Comparison

- Look for local insurers: Sometimes local or regional companies offer lower rates and better service than big brands.

- Review renewal rates: Some companies raise rates after the first year—ask what your renewal price will be.

- Snapshot or telematics programs: Some insurers offer discounts if you let them track your driving for a few weeks. If you’re a safe driver, this can lower your price.

What To Do After You Choose A Policy

Once you pick a policy:

- Review all documents before signing.

- Make your first payment on time to start coverage.

- Download or print your insurance card for your car.

- Save your insurer’s contact details in your phone.

- Set a reminder to compare again next year.

Sample Comparison Scenario

Let’s see how two drivers might compare insurance:

Maria, age 28, drives a 2018 Toyota Corolla, lives in a city, has no accidents.

Tom, age 40, drives a 2015 Ford F-150, lives in a rural area, one accident last year.

Both use an online tool and enter the same coverage limits. Here’s what they find:

| Driver | Lowest Quote | Company | Deductible | Special Features |

|---|---|---|---|---|

| Maria | $820/year | SafeAuto | $500 | Roadside, rental car |

| Tom | $1,250/year | ABC Insurance | $1,000 | Accident forgiveness |

Maria’s city location and clean record give her a lower price, but Tom’s accident and rural area push his cost higher. Both can adjust deductibles or look for discounts to save more.

Real-world Example: Savings From Comparing

According to a 2023 study by NerdWallet, drivers who compare car insurance online at renewal time save an average of $560 per year. This shows the value of taking just a few minutes to check your options.

Frequently Asked Questions

How Often Should I Compare Car Insurance?

You should compare car insurance once a year, or anytime your situation changes (like buying a new car, moving, or having an accident). Rates can change even if your details stay the same.

Does Comparing Car Insurance Online Affect My Credit Score?

No, getting quotes online is considered a soft inquiry and does not hurt your credit score. Only when you buy a policy might the insurer check your credit more deeply.

What If I Find A Cheaper Quote After Renewing My Policy?

You can usually switch at any time, but check for cancellation fees or refund policies. Make sure your new coverage is active before canceling the old one.

Why Do Quotes From Different Sites Sometimes Not Match?

Different sites may use slightly different information or show estimates instead of final quotes. For best results, enter your details carefully and check with the insurer directly if you see big differences.

Is It Safe To Enter My Personal Information On Comparison Sites?

Most major comparison sites are safe, but always check for a secure connection (https://), read privacy policies, and never share payment info unless you are ready to buy.

Choosing car insurance is a big decision, but with the right approach, you can find a policy that fits your needs and budget. Take your time, look past just the price, and use the tips in this guide to compare car insurance online with confidence.

You’ll not only save money—you’ll also get better protection for the road ahead.