How Much Is Honda Civic Car Insurance

Figuring out your car insurance costs can feel tricky, especially if you’re new to it. Many people wonder, How Much Is Honda Civic Car Insurance? It’s a very common question because the price isn’t set in stone; it changes for everyone. Don’t worry, though!

We’ll make it simple and show you exactly what affects your rate. Let’s get started and find out what you can expect for your Honda Civic’s coverage.

Honda Civic Car Insurance Costs Explained

When people ask about the cost of insuring a Honda Civic, they’re looking for a clear answer. The truth is, there’s no single price. Your insurance premium depends on many different things.

We’ll break down the main factors that influence how much you’ll pay. This will help you understand why your quote might be different from someone else’s. It’s about your personal situation and the car itself.

Your Personal Information Matters

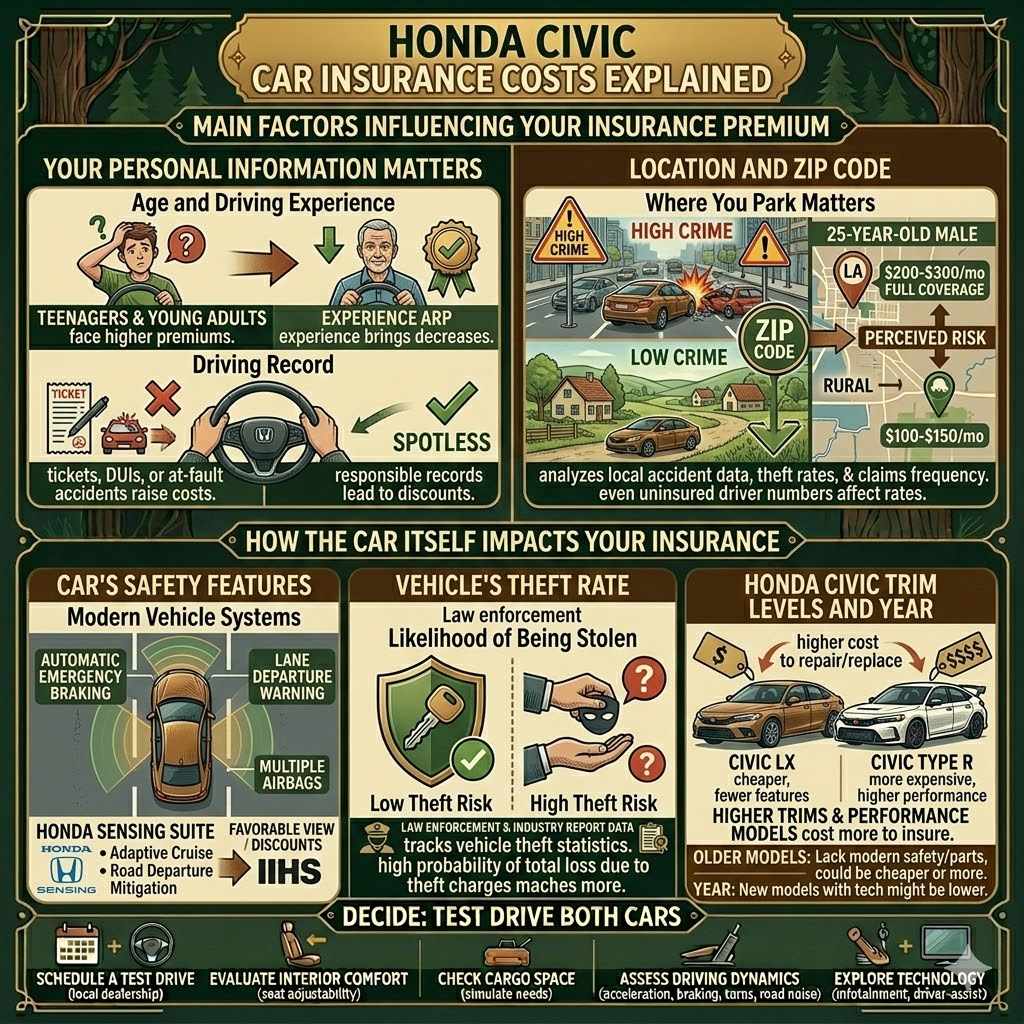

Insurance companies look at who you are when they set your rates. This includes your age, driving history, and where you live. Younger drivers often pay more because they’re seen as riskier.

A clean driving record with no accidents or tickets means lower costs. Your location is also a big deal. Living in a busy city with more car theft or accidents will raise your insurance price.

Age and Driving Experience

Your age plays a significant role in how insurance companies assess risk. Teenagers and young adults typically face higher premiums. This is because statistics show they are more likely to be involved in accidents.

As drivers gain more experience and reach their late twenties or thirties, premiums usually decrease. This trend continues as drivers age, provided they maintain a safe driving record.

Driving Record

Your history behind the wheel is a key factor. A history of speeding tickets, DUIs, or at-fault accidents will increase your insurance costs. Insurers see these as indicators of potential future claims.

Conversely, a spotless record with no violations or claims signals to insurers that you are a responsible driver. This can lead to significant discounts.

Location and Zip Code

Where you park your car each night heavily impacts your insurance rates. Areas with high crime rates, such as car theft or vandalism, or densely populated regions with more traffic congestion, tend to have higher premiums. Insurers analyze local accident data, theft rates, and the frequency of insurance claims in your specific zip code.

Even living in a neighborhood with more uninsured drivers can affect your rates.

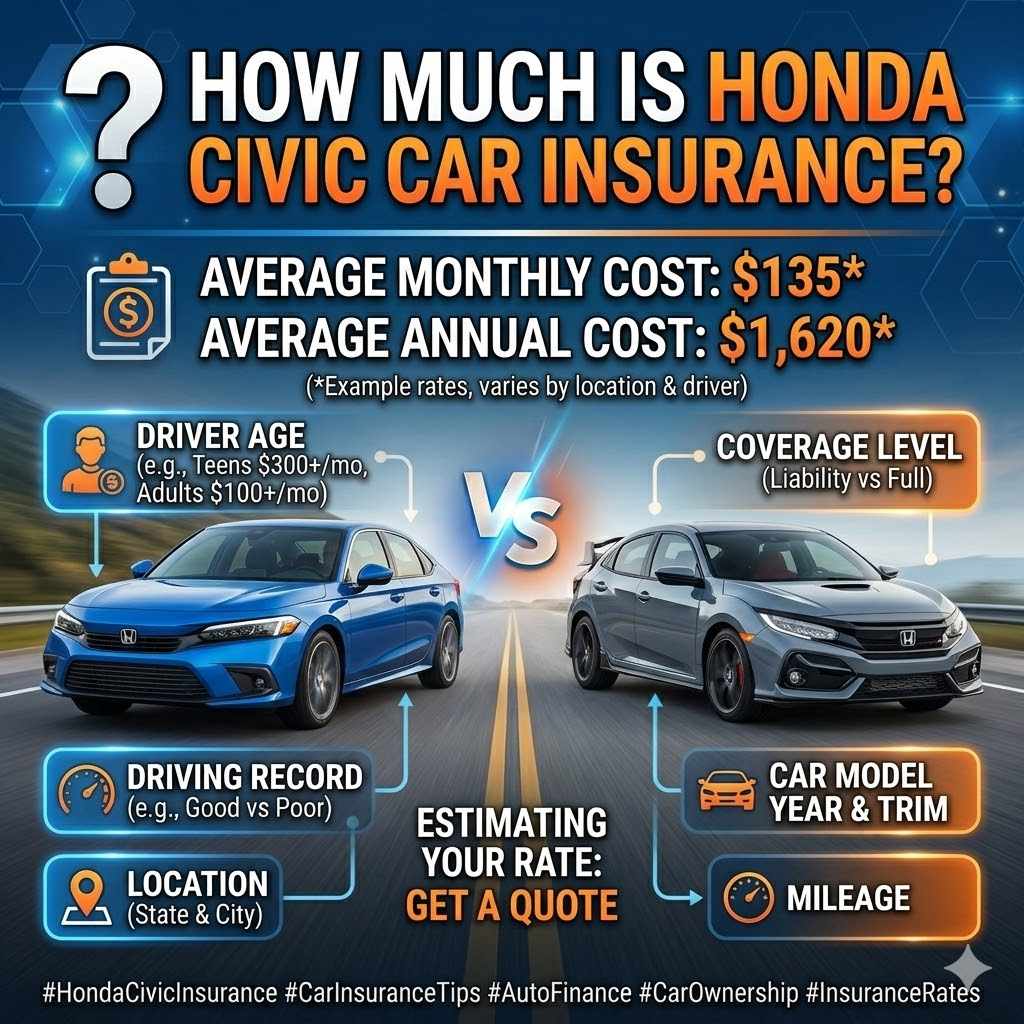

For instance, a 25-year-old male living in a major city like Los Angeles might pay $200-$300 per month for full coverage on a Honda Civic. The same driver, if living in a rural area with low crime and accident rates, might pay $100-$150 per month. This difference is directly tied to the risk perceived by the insurer based on location.

How Much Is Honda Civic Car Insurance Based on the Car

The Honda Civic is a popular car, and its insurance cost is influenced by its specific model and safety features. The year of the car, its trim level, and even its color can play a part. Newer models with advanced safety technology might have lower rates because they are less likely to be stolen or involved in serious accidents.

On the other hand, cars that are frequently stolen might cost more to insure.

Car’s Safety Features

Modern vehicles often come equipped with advanced safety systems. These can include automatic emergency braking, lane departure warnings, and multiple airbags. Insurers view these features favorably because they can help prevent accidents or reduce the severity of injuries.

Cars with higher safety ratings from organizations like the Insurance Institute for Highway Safety (IIHS) often receive discounts on insurance premiums.

For example, a Honda Civic equipped with Honda Sensing, a suite of driver-assistive technologies, might qualify for a discount. This technology includes features like adaptive cruise control and road departure mitigation. These systems are designed to actively help the driver avoid collisions, making the car a safer bet for insurers.

Vehicle’s Theft Rate

The likelihood of a car being stolen is a significant factor in its insurance cost. Some car models are targeted more often by thieves than others. If a particular model, including certain Honda Civic generations or trims, has a high theft rate in your area, your insurance premiums could be higher.

Insurers use data from law enforcement and industry reports to track vehicle theft statistics.

For instance, if a specific year of Honda Civic consistently ranks high on lists of stolen vehicles, insurance companies will charge more to cover it. They factor in the probability of a total loss due to theft. This is why checking the theft statistics for your desired model can be a wise step before purchasing a car.

Honda Civic Trim Levels and Year

The Honda Civic is available in various trim levels, such as LX, EX, Touring, and the sportier Si or Type R models. Higher-end trims with more powerful engines or luxury features often come with a higher price tag. This means they also tend to cost more to insure.

The cost to repair or replace a more expensive model will naturally be higher, translating to higher insurance premiums.

A 2023 Honda Civic LX will likely cost less to insure than a 2023 Honda Civic Type R. The Type R has a more powerful engine, performance-oriented features, and a higher sticker price, all of which contribute to increased insurance costs. Similarly, older models may be cheaper to buy but could cost more to insure if parts are harder to find or if they lack modern safety features.

Types of Honda Civic Insurance Coverage

The amount you pay for Honda Civic insurance also depends heavily on the types and amounts of coverage you choose. Think of it as picking what you want to be protected by. If you want the most protection, it will likely cost more.

Understanding these options helps you make informed decisions about your policy.

Liability Coverage

This is the most basic type of coverage and is required by law in most places. It covers damages and injuries you cause to others if you are at fault in an accident. Liability coverage has two parts: bodily injury liability and property damage liability.

Bodily injury covers medical expenses for others, and property damage covers damage to their vehicles or property. Higher liability limits will increase your premium but offer greater financial protection.

For example, if you have the state minimum liability coverage and cause an accident where someone is seriously injured and their car is totaled, your insurance might not cover all the costs. This means you could be personally responsible for the remaining expenses, which could be tens of thousands of dollars or more. Choosing higher limits, like $100,000/$300,000 bodily injury and $100,000 property damage, offers better protection.

Collision Coverage

Collision coverage helps pay to repair or

A higher deductible means you pay more out of pocket if you file a claim, but your monthly premium will be lower. For example, choosing a $1,000 deductible instead of a $500 deductible on collision coverage can significantly reduce your insurance premium. However, you must be prepared to pay that higher amount if you need to file a claim.

Comprehensive Coverage

Comprehensive coverage helps pay for damages to your Honda Civic that are not caused by a collision. This includes things like theft, vandalism, fire, natural disasters (hail, floods, etc.), and falling objects. Like collision coverage, it is optional if you own your car outright but usually required by lenders.

It also comes with a deductible.

A common scenario where comprehensive coverage is essential is if your car is damaged by a falling tree branch during a storm. Without comprehensive coverage, you would have to pay for the repairs entirely out of pocket. With it, your insurance company would cover the cost, minus your deductible.

The theft of a car is also covered under comprehensive insurance.

Uninsured and Underinsured Motorist Coverage

This coverage protects you if you’re in an accident with a driver who has no insurance or not enough insurance to cover your damages. Uninsured motorist (UM) coverage can help pay for your medical bills and, in some states, damage to your car. Underinsured motorist (UIM) coverage steps in when the at-fault driver’s insurance isn’t enough to cover your losses.

Imagine you’re hit by a driver who only has the minimum liability coverage required by their state, say $25,000. If your medical bills total $50,000, your own underinsured motorist coverage could pay the remaining $25,000. This is crucial protection, as many drivers carry only the bare minimum coverage or none at all.

Other Optional Coverages

Many other optional coverages can affect your overall premium. These might include roadside assistance, rental car reimbursement, and new car

For example, if your Honda Civic is stolen and declared a total loss, and you have new car replacement coverage, you could get a brand-new Civic. If you only have standard comprehensive coverage, you would receive the depreciated cash value of your stolen car, which might not be enough to buy an exact replacement.

How to Get the Best Rate for Honda Civic Insurance

Now that you understand what affects your Honda Civic insurance costs, let’s talk about how to get the best possible rate. It’s not just about the car or your personal details; it’s also about smart shopping and taking advantage of discounts. Here are some effective strategies you can use.

Shop Around and Compare Quotes

This is perhaps the most important step. Insurance rates can vary significantly from one company to another for the exact same coverage. Don’t just accept the first quote you receive.

Get quotes from at least three to five different insurance providers. This includes national companies and local agents.

For example, you might get a quote for full coverage on a 2020 Honda Civic EX for $150 per month from Company A, $180 from Company B, and $130 from Company C. By comparing, you can save $20 to $50 per month, which adds up to $240 to $600 per year. Use online comparison tools or call agents directly to gather these quotes.

Take Advantage of Discounts

Insurance companies offer a wide array of discounts to reward safe and responsible policyholders. Make sure you ask about every discount you might be eligible for. Common discounts include safe driver discounts, good student discounts (for younger drivers), multi-policy discounts (bundling auto and home insurance), and discounts for safety features in your car.

A typical multi-car discount might save you 10-20% off your premium. Bundling your auto and homeowners insurance with the same company could offer an additional 5-15% discount on each policy. These savings can be substantial over time, making your insurance more affordable.

Ask your agent about discounts for things like paperless billing or paying your premium in full.

Consider Raising Your Deductible

As mentioned earlier, choosing a higher deductible for your collision and comprehensive coverage can lower your monthly premiums. However, it’s crucial to ensure you can afford to pay the higher deductible amount if you need to file a claim. A balance is key here; don’t set a deductible so high that it would cause financial hardship.

If you currently have a $500 deductible and are paying $160 per month for full coverage, you might consider raising it to $1,000. This could potentially lower your monthly premium to $130 or $140. This would save you $20-$30 per month, or $240-$360 per year, but you would need to have $1,000 readily available in case of an accident.

Maintain a Good Driving Record

This is one of the most effective ways to keep your insurance costs low. Avoid traffic violations, speeding tickets, and any at-fault accidents. Most insurance companies offer a “safe driver discount” if you have a clean record for a certain period, often three to five years.

They may also offer a “claims-free discount.”

A safe driver discount can range from 10% to 25% off your premium. For example, if your annual premium is $1,200, a 15% safe driver discount would save you $180 per year. This discount is often automatically applied once you qualify, but it’s always good to confirm with your insurer.

Drive Less

If you don’t drive your Honda Civic very often, you might be eligible for a low-mileage discount. Some insurers offer specific programs for drivers who commute less than a certain number of miles per year. Telematics devices or apps can track your driving habits and mileage, potentially leading to lower rates if you prove you’re a safe and infrequent driver.

For instance, if you only drive 5,000 miles a year instead of the national average of 13,500 miles, you could qualify for a discount. This discount might be anywhere from 5% to 15% of your premium. This is especially relevant for individuals who work from home or use public transportation frequently.

Factors Influencing Honda Civic Insurance Rates

Understanding the specific characteristics of the Honda Civic can help demystify its insurance costs. Insurers assess various aspects of the vehicle itself. These include its safety ratings, repair costs, and overall value.

These elements combine with your personal factors to determine your premium.

Safety Ratings and Crash Test Performance

The Honda Civic consistently receives high safety ratings from organizations like the National Highway Traffic Safety Administration (NHTSA) and the Insurance Institute for Highway Safety (IIHS). A car’s safety performance is a major indicator for insurers. Vehicles that perform well in crash tests and offer good occupant protection are generally seen as less risky.

For example, many Honda Civic models have earned an “Overall 5-Star Safety Rating” from NHTSA, its highest possible score. IIHS often rates the Civic as a “Top Safety Pick” or “Top Safety Pick+”. This means fewer potential medical claims for injuries, which translates into lower insurance premiums for the owner.

Cost of Parts and Repair

The availability and cost of parts for repairs are significant factors in determining insurance premiums. The Honda Civic is a mass-produced vehicle with widely available and relatively affordable parts. This makes repairs less expensive for insurance companies compared to luxury or exotic cars with hard-to-find and costly components.

A common repair for a fender bender on a Honda Civic might involve replacing a bumper cover, headlight assembly, and potentially some body panels. The cost for these parts and the labor to install them is generally lower than for a car from a premium brand. This efficiency in repair helps keep insurance costs for the Civic manageable.

Vehicle Value and Depreciation

The overall market value of your Honda Civic directly impacts the cost of comprehensive and collision coverage. Newer models with higher price tags naturally cost more to insure than older models. However, the Civic is known for holding its value well, meaning it depreciates slower than some other vehicles.

This can be a double-edged sword: higher value means higher insurance, but good resale value means less of a total loss for the insurer if the car is totaled.

A 2023 Honda Civic Touring, with a manufacturer’s suggested retail price (MSRP) of around $30,000, will cost more to insure for comprehensive and collision than a 2015 Honda Civic LX valued at $10,000. Insurers base these coverages on the replacement cost of the vehicle, minus your deductible.

Fuel Efficiency and Engine Type

While not as direct a factor as safety or value, fuel efficiency and engine type can sometimes indirectly influence insurance rates. Cars with more powerful engines might be driven more aggressively, potentially leading to a higher risk of accidents. However, for a popular model like the Honda Civic, the impact is often minimal, especially when compared to other factors.

For instance, while the standard Civic engines are known for their fuel economy and reliability, the sportier Si or Type R variants have more powerful turbocharged engines. These models might carry slightly higher premiums due to their performance-oriented nature, which could correlate with a higher likelihood of aggressive driving or being involved in higher-speed incidents.

Theft Risk

As mentioned before, the theft risk associated with a specific car model is a major consideration for insurers. While the Honda Civic is generally a very popular and reliable car, certain model years or trim levels might be more attractive to thieves. Insurers use data from various sources to assess this risk for each vehicle.

If a particular generation of Honda Civic has been identified as a frequent target for car thieves in certain regions, insurance companies will adjust their premiums accordingly. They might also offer discounts if the vehicle is equipped with an anti-theft device, such as a factory-installed alarm or an aftermarket tracking system.

| Coverage Type | Description | Impact on Cost |

|---|---|---|

| Liability | Covers damage/injury to others | Required; Higher limits increase cost |

| Collision | Covers damage to your car in an accident | Optional; Higher deductible lowers cost |

| Comprehensive | Covers non-collision damage (theft, weather) | Optional; Higher deductible lowers cost |

| UM/UIM | Protects against uninsured/underinsured drivers | Optional; Adds to cost, provides crucial protection |

Frequently Asked Questions

Question: How much does full coverage for a Honda Civic typically cost per year?

Answer: Full coverage for a Honda Civic can range anywhere from $1,200 to $2,500 or more per year. This depends heavily on your location, driving record, the specific model year and trim of the Civic, and the coverage limits you select. It’s best to get personalized quotes.

Question: Is the Honda Civic considered an expensive car to insure?

Answer: Generally, no. The Honda Civic is known for being relatively affordable to insure compared to sports cars or luxury vehicles. Its good safety ratings, common parts availability, and reasonable repair costs contribute to lower premiums.

Question: Does my credit score affect my car insurance rates for a Honda Civic?

Answer: Yes, in most states, your credit-based insurance score can affect your rates. Insurers use credit history as a predictor of risk. A good credit score often leads to lower insurance premiums for your Honda Civic.

Question: What is the cheapest way to insure a Honda Civic?

Answer: To get the cheapest insurance, shop around for quotes, consider higher deductibles, ask for all applicable discounts, maintain a clean driving record, and drive fewer miles. Bundling policies can also help reduce costs.

Question: Will adding a young driver to my Honda Civic insurance significantly increase the cost?

Answer: Yes, adding a young or inexperienced driver typically causes a substantial increase in insurance costs. Their lack of driving history is seen as higher risk by insurers. You might consider adding them to a policy with lower coverage limits initially if possible, but always prioritize adequate protection.

Conclusion

Understanding How Much Is Honda Civic Car Insurance? involves looking at your personal details, the car’s specifics, and your chosen coverage. By comparing quotes, using discounts, and driving safely, you can find affordable rates. Your Honda Civic is a smart choice, and insuring it doesn’t have to be complicated.

Get your personalized quotes today.