Figuring out how much you’ll pay each month for a Honda Civic can feel a bit tricky when you’re new to buying a car. Lots of things go into that number, and it’s easy to get lost in all the details. But don’t worry!

This guide will break down How Much Is a Honda Civic Car Payment? into simple steps. We’ll show you exactly what to look for so you can get a clear picture of your monthly costs. Get ready to feel confident about your car financing.

Understanding Honda Civic Car Payment Factors

The price you pay each month for a Honda Civic depends on several key things. It’s not just a single number that applies to everyone. Think of it like building with blocks; each block adds to your total.

Knowing these building blocks helps you predict what your payment might look like.

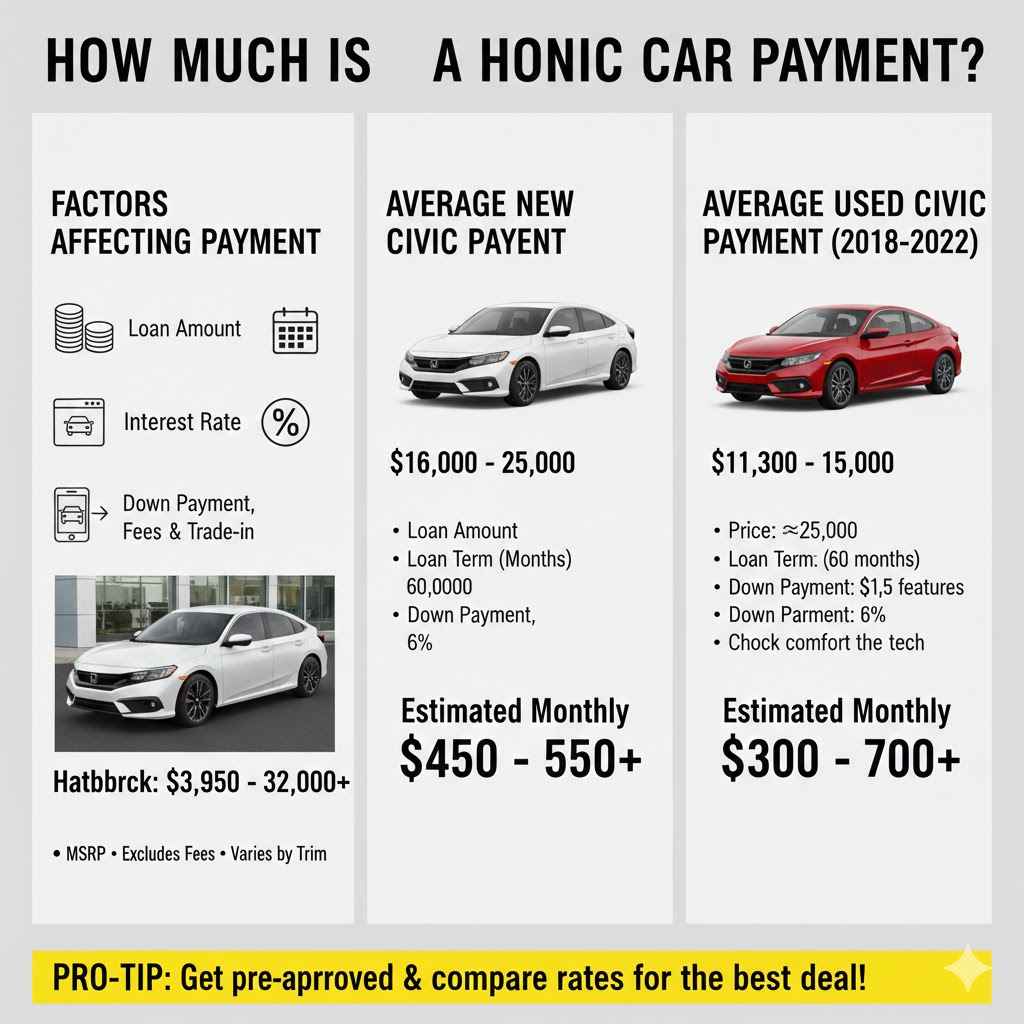

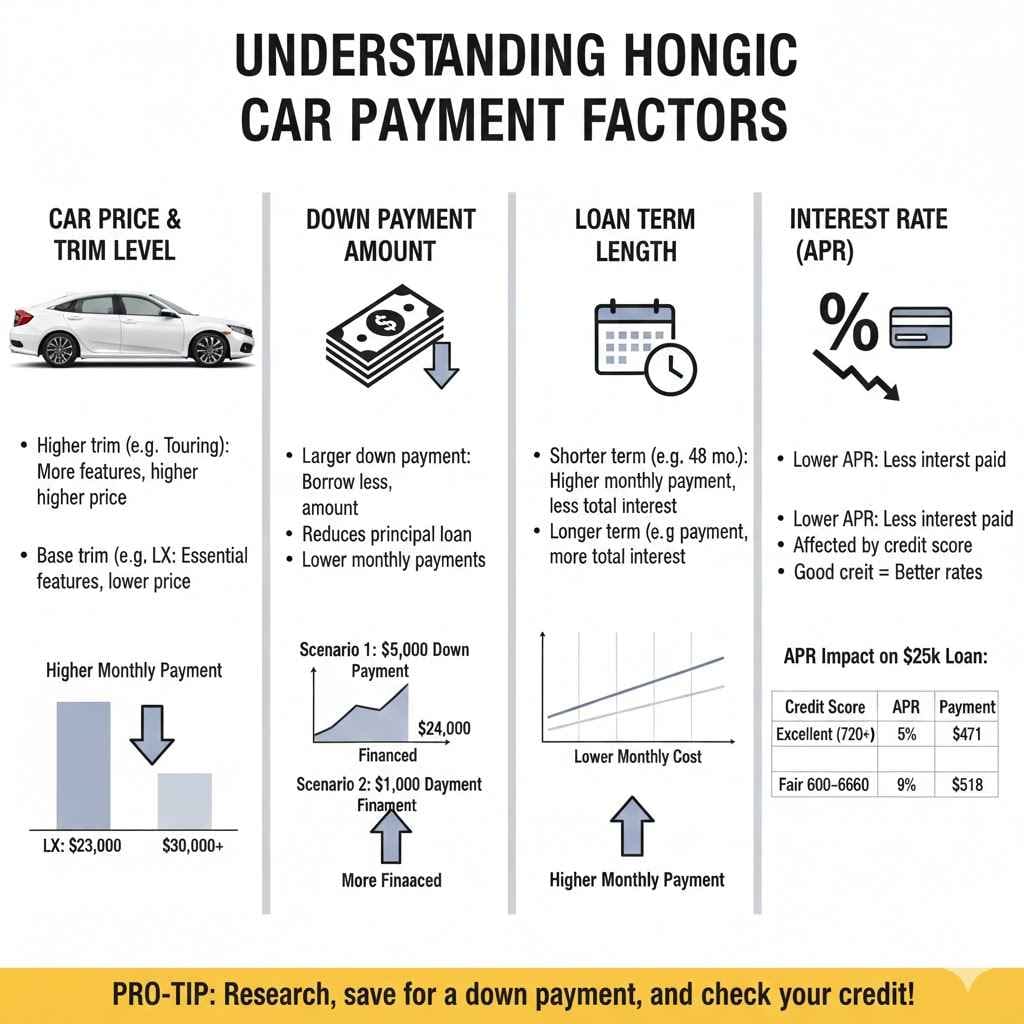

Car Price And Trim Level

The starting point for any car payment is the price of the car itself. Honda Civics come in different models, called trim levels, like the LX, Sport, EX, and Touring. Each trim offers more features and technology.

A higher trim level, with more advanced features and a better engine, will cost more than a basic trim. This higher sticker price directly leads to a larger loan amount and, consequently, a higher monthly payment.

For example, a base model Honda Civic LX might have a starting MSRP of around $23,000. A top-tier Honda Civic Touring, loaded with premium features, could start closer to $30,000. This difference of several thousand dollars significantly impacts the monthly car payment over the life of the loan.

Down Payment Amount

When you buy a car, you can choose to pay a portion of the car’s price upfront. This is called a down payment. A larger down payment means you borrow less money.

Borrowing less money means your monthly payments will be lower. Some people put down 5% of the car’s price, while others might put down 20% or even more. A down payment helps reduce the principal loan amount, which is the amount you finance.

If you buy a $25,000 Civic and make a $5,000 down payment, you will only need to finance $20,000. If you only put down $1,000, you would need to finance $24,000. This $4,000 difference in financed amount can save you hundreds or even thousands of dollars in interest over time, lowering your monthly cost.

Loan Term Length

The loan term is how long you have to pay back the money you borrowed for the car. Car loans can range from 36 months (3 years) to 84 months (7 years). A shorter loan term means you pay more each month, but you pay less interest overall because you’re paying off the loan faster.

A longer loan term means you pay less each month, but you’ll end up paying more interest over the life of the loan.

For instance, a 48-month loan will have a higher monthly payment than a 72-month loan for the same amount borrowed. However, the total interest paid on the 48-month loan will be considerably less than on the 72-month loan. It’s a trade-off between a lower immediate monthly cost and a lower total cost in the long run.

Interest Rate (APR)

The interest rate, often shown as Annual Percentage Rate (APR), is the cost of borrowing money. It’s expressed as a percentage of the loan amount. A lower APR means you pay less in interest on your loan.

Your credit score plays a huge role in the APR you’ll be offered. People with excellent credit scores usually get the lowest interest rates.

Lenders look at your credit history to decide how risky it is to lend you money. A good credit score shows you’re a reliable borrower, so they offer you a better interest rate. A lower APR can significantly reduce your monthly payment and the total amount of interest you pay over the loan’s duration.

For example, a 1% difference in APR can mean hundreds of dollars saved over a five-year loan.

Additional Fees And Taxes

Beyond the car price, loan interest, and down payment, there are other costs to consider. These include sales tax, registration fees, and potential dealer fees. Sales tax varies by state and county.

Registration fees are also state-dependent. These fees are usually rolled into the total loan amount, increasing the principal you need to finance. This increase will, in turn, affect your monthly payment.

Always ask for a breakdown of all fees before signing any paperwork.

Calculating Your Potential Honda Civic Car Payment

Now that you know what factors influence your payment, let’s look at how to estimate it. You don’t need to be a math whiz to get a good idea. We’ll use a common method and a handy tool to help.

Using A Car Loan Calculator

The easiest way to estimate your monthly Honda Civic car payment is by using an online car loan calculator. These tools are available on many car dealership websites, bank sites, and general financial advice sites. They are designed to be very user-friendly.

You simply input the car’s price, your expected down payment, the loan term (in months), and the estimated interest rate (APR). The calculator then does the work and shows you an estimated monthly payment. This is a great first step to see what you can afford.

Sample Scenario Using a Calculator:

- Car Price: $25,000 (for a Honda Civic EX)

- Down Payment: $3,000

- Loan Term: 60 months (5 years)

- Estimated APR: 6.0%

Plugging these numbers into a typical car loan calculator would show an estimated monthly payment of around $405. This figure doesn’t include taxes and fees, which would add a bit more.

Understanding The Math Behind The Calculator

While calculators are easy, knowing the basic math can help you trust the numbers. Car loan payments are calculated using a loan amortization formula. This formula determines how much of each payment goes towards the principal (the amount borrowed) and how much goes towards interest.

The formula looks a bit complex, but it essentially balances the loan amount, interest rate, and loan term to find a consistent monthly payment. The longer the loan term and the higher the interest rate, the more you’ll pay in total interest over time. This is why lenders and financial advisors often suggest the shortest loan term you can comfortably afford, alongside the lowest possible APR.

The formula for calculating a fixed monthly payment (M) is:

M = P /

Where:

- P = Principal loan amount (car price minus down payment)

- i = Monthly interest rate (annual interest rate divided by 12)

- n = Total number of payments (loan term in years multiplied by 12)

For example, if P = $20,000, annual APR = 6%, and term = 60 months (5 years):

- Monthly interest rate (i) = 0.06 / 12 = 0.005

- Total number of payments (n) = 60

- M = 20000 /

- M = 20000 /

- M = 20000 /

- M = 20000 /

- M = 134.885 / 0.34885

- M ≈ $386.67

This calculation is for the principal and interest only. Taxes and fees would increase this amount.

Factors Affecting Your Interest Rate

Your interest rate, or APR, is a huge piece of the payment puzzle. Even a small difference in percentage can add up significantly over several years. Lenders use your financial history to decide what rate to offer you.

Credit Score Importance

Your credit score is a three-digit number that tells lenders how likely you are to repay borrowed money. It’s based on your history of paying bills, the amount of debt you have, and how long you’ve had credit. A higher credit score, generally above 700, signals to lenders that you are a low-risk borrower.

This typically results in a lower interest rate. For example, someone with a credit score of 780 might get an APR of 5%, while someone with a score of 620 might be offered an APR of 9%.

The difference between 5% and 9% APR on a $25,000 loan over 60 months is substantial. At 5% APR, the monthly payment is about $481, with total interest of $3,860. At 9% APR, the monthly payment jumps to about $526, with total interest of $6,560.

That’s nearly $2,700 more in interest paid.

Loan To Value Ratio

The loan-to-value (LTV) ratio compares the amount of money you’re borrowing to the value of the car. It’s calculated by dividing the loan amount by the car’s market value. For example, if you want to borrow $25,000 for a car valued at $30,000, your LTV is about 83% ($25,000 / $30,000).

A lower LTV ratio generally means a lower risk for the lender, which can lead to a better interest rate.

Lenders often prefer LTV ratios below 80%. This means they like to see a down payment that makes the loan amount less than 80% of the car’s value. If you make a larger down payment, you lower your LTV ratio.

This can make you a more attractive borrower and potentially help you secure a more favorable APR. For instance, a $5,000 down payment on a $30,000 car lowers the LTV to 83.3%. If you put down $7,000, the LTV drops to 76.7%, which is more appealing to lenders.

Relationship With Lender

Sometimes, your existing relationship with a bank or credit union can influence your interest rate. If you have a long history of responsible borrowing and banking with a particular institution, they might be willing to offer you a slightly better APR as a loyal customer. This could be a small discount or a more flexible loan term.

For example, if you have been banking with Credit Union A for 10 years and have always managed your accounts well, they might offer you a special rate on a car loan. This could be a perk of being a valued member. Building a positive financial history with your bank or credit union can pay off in various ways, including better loan terms.

Tips For Lowering Your Honda Civic Car Payment

You can take several steps to make your monthly Honda Civic payment more affordable. Planning ahead and making smart choices are key. Here are some practical tips to help you save money.

Shop Around For Financing

Don’t just accept the first loan offer you get from a dealership. Banks, credit unions, and online lenders all compete for your business. Getting pre-approved for a loan from multiple sources before you visit the dealership gives you leverage.

You can compare the APRs, fees, and terms offered by each lender. This allows you to choose the loan that offers the best value for your specific situation.

Example Scenario:

- You get pre-approved at Bank A for a 60-month loan at 7.5% APR.

- You also get pre-approved at Credit Union B for a 60-month loan at 7.0% APR.

- The dealership’s financing department offers you a 60-month loan at 8.0% APR.

In this case, Credit Union B offers the lowest interest rate. By shopping around, you could save money each month and over the life of the loan.

Negotiate The Price Of The Car

The sticker price of the car is a major factor in your loan amount. Don’t be afraid to negotiate the purchase price of the Honda Civic. Research the market value of the specific trim and model you’re interested in.

Use resources like Kelley Blue Book or Edmunds to find out what others are paying in your area. A successful negotiation can lower the car’s price, which in turn lowers the amount you need to finance.

This negotiation happens before you talk about financing. A lower car price means a smaller loan, leading to lower monthly payments and less interest paid overall. For instance, if you negotiate $1,500 off the price of a $27,000 Civic, you’re now looking at financing $25,500 instead of $27,000, assuming the same down payment.

This reduction can shave off dollars from your monthly bill.

Consider A Used Honda Civic

New cars depreciate rapidly in their first few years. A pre-owned Honda Civic, especially one that is only a few years old, can offer significant savings. Used cars have already gone through their steepest depreciation curve, meaning they hold their value better relative to their purchase price.

This lower purchase price directly translates to a smaller loan and a more affordable monthly payment. You can often find well-maintained, low-mileage used Civics for considerably less than their brand-new counterparts.

For example, a 3-year-old Honda Civic might be priced 20-30% lower than the same model when it was new. This can make a big difference in your monthly payment and the total interest paid over the life of the loan. It allows you to get a great car without the “new car” premium.

Make A Larger Down Payment

As mentioned earlier, a larger down payment reduces the amount you need to finance. If you can save up more money to put down, it’s one of the most effective ways to lower your monthly car payment. Even an extra $1,000 or $2,000 can make a noticeable difference.

The more equity you have in the car from the start, the less you borrow, and the less interest you will pay.

Think about it this way: if you’re looking at a $25,000 car and can save an extra $2,000 for a down payment, your loan amount drops by $2,000. Over a 5-year loan with a 6% APR, this $2,000 reduction can save you approximately $160 in interest and lower your monthly payment by around $33. Small savings add up.

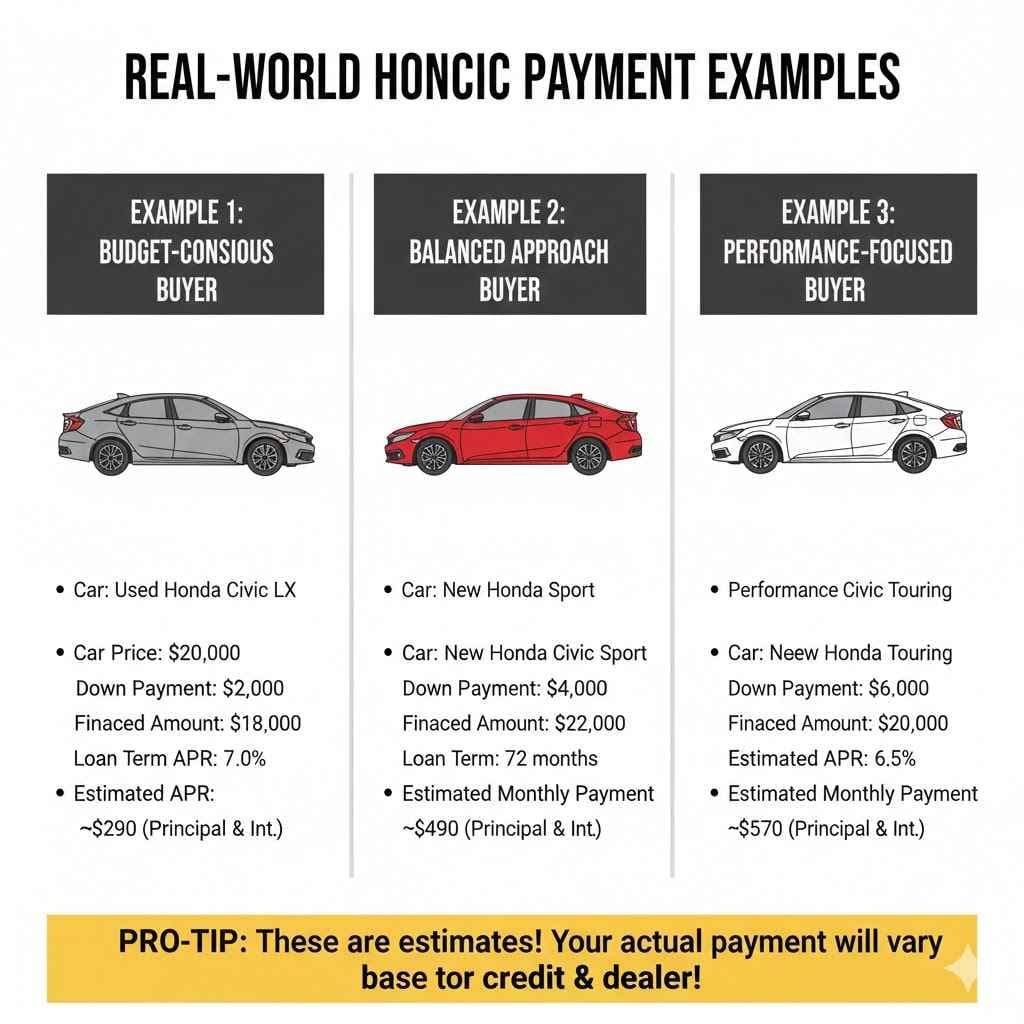

Real-World Honda Civic Payment Examples

To give you a clearer picture, let’s look at some hypothetical scenarios for different budgets and loan situations. These examples will help you see how the factors we’ve discussed play out in real payments. Remember, these are estimates and actual figures may vary based on your specific credit, location, and chosen dealer.

Example 1: Budget-Conscious Buyer

This buyer is focused on keeping the monthly payment as low as possible, prioritizing affordability over the latest features.

- Car: Used Honda Civic LX (2 years old)

- Car Price: $20,000

- Down Payment: $2,000

- Amount to Finance: $18,000

- Loan Term: 72 months (6 years)

- Estimated APR: 7.0%

Estimated Monthly Payment: Approximately $290 (Principal & Interest only)

This buyer chose a slightly older model and a longer loan term to achieve a low monthly payment. They will pay more interest over time but have a more manageable monthly expense. This is a common strategy for those on a tight budget.

Example 2: Balanced Approach Buyer

This buyer wants a newer car with more features but still aims for a reasonable monthly payment.

- Car: New Honda Civic Sport

- Car Price: $26,000

- Down Payment: $4,000

- Amount to Finance: $22,000

- Loan Term: 60 months (5 years)

- Estimated APR: 6.0%

Estimated Monthly Payment: Approximately $415 (Principal & Interest only)

This buyer opted for a new car and a standard 5-year loan. They have a good balance between a modern vehicle and a payment that is not excessively high. The interest rate is also quite good, keeping the total cost down.

Example 3: Performance-Focused Buyer

This buyer is interested in a higher trim level and is willing to accept a slightly higher payment for more advanced features and performance.

- Car: New Honda Civic Touring

- Car Price: $31,000

- Down Payment: $6,000

- Amount to Finance: $25,000

- Loan Term: 48 months (4 years)

- Estimated APR: 5.5%

Estimated Monthly Payment: Approximately $570 (Principal & Interest only)

This buyer chose the top-tier model and a shorter loan term. They are paying off the car faster, which means less interest paid overall. The monthly payment is higher, reflecting the more expensive car and shorter repayment period.

Frequently Asked Questions

Question: What is the average car payment for a Honda Civic?

Answer: The average car payment for a Honda Civic can vary greatly, but based on typical prices, loan terms, and interest rates, a new Civic could range from about $350 to $600 or more per month, not including taxes and fees. Used Civics will generally have lower payments.

Question: How much down payment is recommended for a Honda Civic?

Answer: While not always required, putting down 10-20% of the car’s price is often recommended. This helps reduce your loan amount, lower your monthly payments, and can potentially get you a better interest rate.

Question: Can I get a Honda Civic car payment under $300 a month?

Answer: It’s possible, especially if you are looking at a used Honda Civic, make a substantial down payment, or secure a very low interest rate with a longer loan term (like 72 or 84 months). However, a brand new Civic typically has a monthly payment higher than $300.

Question: Does the color of a Honda Civic affect the car payment?

Answer: No, the color of the Honda Civic does not affect the car payment. Car payments are based on the price of the car, the loan amount, the interest rate, and the loan term, not cosmetic features like color.

Question: What happens if I can no longer afford my Honda Civic car payment?

Answer: If you struggle to afford your payment, contact your lender immediately. They may offer options like loan modification, deferment, or refinancing. If you can’t find a solution, you might consider selling the car or trading it in to avoid further financial issues like repossession.

Summary

Calculating How Much Is a Honda Civic Car Payment? involves looking at the car’s price, your down payment, the loan length, and the interest rate. Using a car loan calculator is the easiest way to get an estimate. Remember to shop for financing, negotiate the car’s price, and consider a used model or a larger down payment to keep your monthly costs down.

You have the tools to find a payment that fits your budget.