The average monthly car payment for a Honda Civic usually falls between $350 and $550, depending on the model year, financing term, interest rate, and your down payment. We will break down the proven factors that determine your real-world monthly cost.

Trying to figure out what a Honda Civic will cost you each month can feel like solving a puzzle. You see great prices advertised, but your actual payment seems different. It’s frustrating when you want a reliable car like the Civic but aren’t sure how to budget for the loan. Don’t worry, this is very common! We are going to walk through exactly what makes up that monthly number. By looking at real examples and simple numbers, you’ll know exactly how to calculate your own best estimate. Let’s demystify the monthly payment so you can drive away confidently.

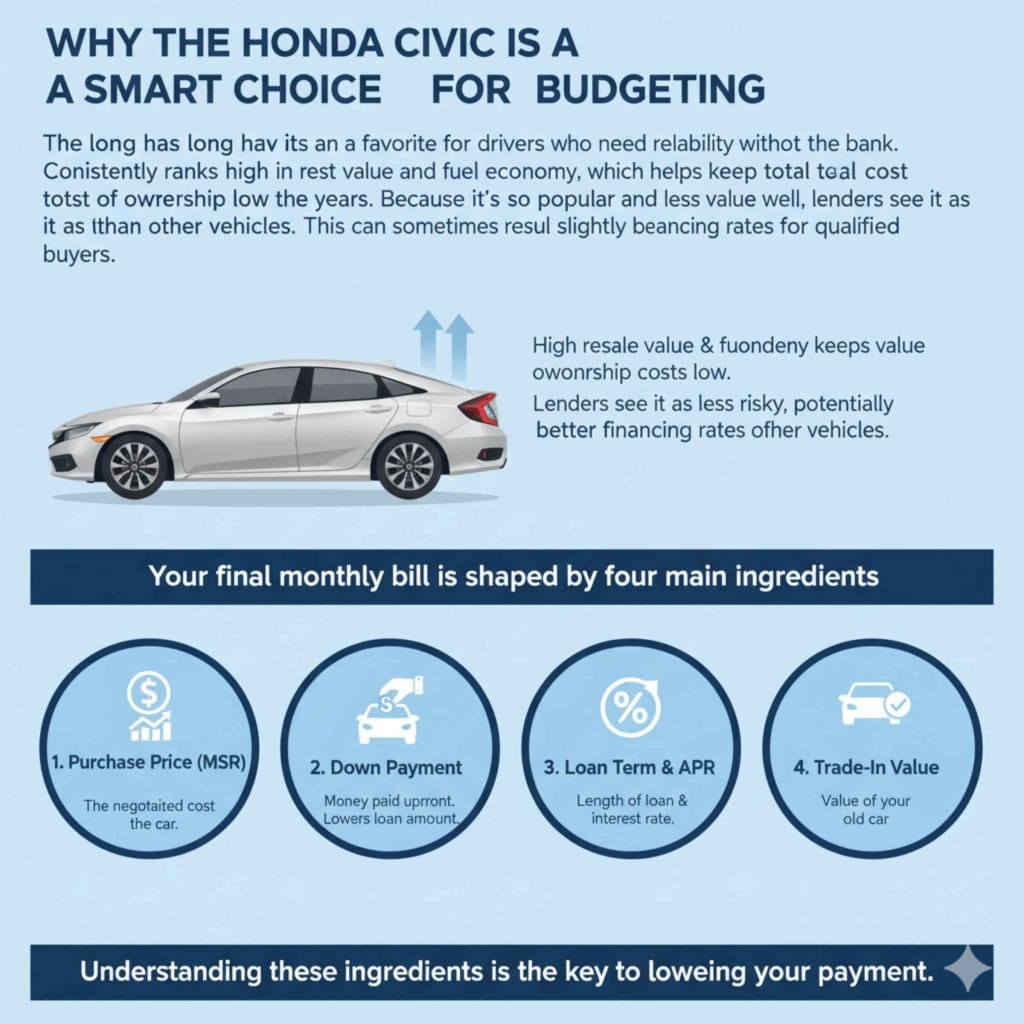

Why the Honda Civic is a Smart Choice for Budgeting

The Honda Civic has long been a favorite for drivers who need reliability without breaking the bank. It consistently ranks high in resale value and fuel economy, which helps keep the total cost of ownership low across the years. Because it’s so popular and holds its value well, lenders often see it as less risky than other vehicles. This can sometimes result in slightly better financing rates for qualified buyers.

Before we dive into the dollar amounts, remember that the sticker price is just the start. Your final monthly bill is shaped by four main ingredients. Understanding these ingredients is the key to lowering your payment.

The Four Critical Factors That Set Your Monthly Payment

Your monthly payment isn’t just based on the sticker price; it’s calculated using a loan formula. Think of these four factors as the levers you can pull to change how much cash leaves your bank account every month.

1. The Price of the Honda Civic (The Principal)

This is the starting point—the actual cost of the car you choose. Civic models vary widely in price, from the basic LX sedan to the sporty Si or the high-performance Type R, or even used models.

- New 2024 Honda Civic Sedan (Base LX): Prices often start around $24,000 before taxes and fees.

- Popular Trims (EX, Touring): These sit comfortably in the $27,000 to $31,000 range.

- Used Civics (3-5 years old): Depending on mileage, you might find these from $18,000 to $24,000.

Dustin’s Tip: Always separate the car price (MSRP) from the “Out-the-Door” Price. The Out-the-Door price includes taxes, title, registration fees, and dealer add-ons. Your loan amount is based on this total out-the-door price.

2. Your Down Payment

A down payment is the cash you pay upfront. Every dollar you put down reduces the amount you need to borrow (the principal). This is one of the most direct ways to lower your monthly payment.

- If a Civic costs $25,000 and you put down $3,000, you are only financing $22,000.

- Putting down more money shortens the loan term needed to pay it off, saving you money on interest over the life of the loan.

3. The Loan Term Length (Months)

The loan term is how long you agree to pay the lender—usually 36, 48, 60, or 72 months. Longer terms mean smaller monthly payments, but you pay more interest overall.

Here is a simple breakdown of the trade-off:

| Loan Term (Months) | Monthly Payment Impact | Total Interest Paid |

|---|---|---|

| 36 Months (3 Years) | Highest Monthly Payment | Lowest Total Interest |

| 60 Months (5 Years) | Moderate Monthly Payment | Medium Total Interest |

| 72 Months (6 Years) | Lowest Comfortable Payment | Highest Total Interest Paid |

4. The Interest Rate (APR)

The Annual Percentage Rate (APR) is the cost of borrowing the money. This factor is heavily dependent on your credit score. A great credit score (typically 740+) makes you eligible for lower rates, which directly lowers your payment compared to someone with fair credit.

For example, a 1% difference in APR on a $25,000 loan over 60 months can easily mean the difference of $20 to $30 per month!

You can check current average new car loan rates based on credit tier provided by reputable financial sources like Bankrate for current industry standards.

Calculating Example Payments for a Honda Civic

To give you a realistic idea of how much is a car payment for a Honda Civic, let’s run a few common scenarios. These are estimates based on current market conditions. Remember, these examples use the principal and interest only—they do not include sales tax, which varies by state.

Scenario 1: The Budget-Conscious Buyer (Used Civic)

This buyer targets a reliable, slightly older Honda Civic to keep costs low.

- Vehicle Price (Loan Amount): $19,000

- Down Payment: $2,000

- Net Amount Financed: $17,000

- Credit Score: Good (Approx. 680 APR)

- Loan Term: 60 Months (5 Years)

Estimated Payment for Scenario 1:

Using standard loan calculators, the resulting payment is typically around $335 per month.

Scenario 2: The Average New Buyer (New LX Sedan)

This is the most common scenario: financing a brand-new, entry-level Civic.

- Vehicle Price (Loan Amount): $24,500 (MSRP + Fees)

- Down Payment: $3,000

- Net Amount Financed: $21,500

- Credit Score: Excellent (Approx. 5.5% APR)

- Loan Term: 60 Months (5 Years)

Estimated Payment for Scenario 2:

This budget-friendly new Civic results in a payment around $410 per month.

Scenario 3: Upscale Trim with a Longer Term

This buyer wants a higher trim level (like an EX or Sport) but wants the lowest possible monthly payment.

- Vehicle Price (Loan Amount): $28,000 (Higher Trim)

- Down Payment: $1,000

- Net Amount Financed: $27,000

- Credit Score: Average (Approx. 7.0% APR)

- Loan Term: 72 Months (6 Years)

Estimated Payment for Scenario 3:

Stretching the loan to six years results in a payment near $440 per month, even though you finance more and pay more interest overall.

Comparing the Real-World Cost of New vs. Used Civics

The age of the car makes a huge difference in your final payment, safety features, and warranty coverage. Let’s look closer at the trade-offs.

| Feature Area | New Honda Civic Payment | Used Honda Civic Payment (3-5 Y.O.) |

|---|---|---|

| Typical Monthly Range | $380 – $550 | $300 – $420 |

| APR Expectation | Usually lower (especially with incentives) | Slightly higher, depending on financing source |

| Warranty Coverage | Full Bumper-to-Bumper & Powertrain | Likely expired or limited extended coverage |

| Depreciation Hit | Fastest in the first 3 years | Slower depreciation curve; more stable value |

| Insurance Cost | Generally higher | Generally lower |

When you buy new, you are paying a premium for the latest tech and the peace of mind of a full factory warranty. When you buy used, you are saving significantly on the principal, leading to a lower payment, but you might take on more immediate maintenance costs later on.

Simple Steps to Lower Your Actual Honda Civic Payment Today

If the estimates above are higher than your ideal budget, take heart. You have control over three of the four main factors. Follow these simple steps to chip away at that monthly payment.

Step 1: Boost Your Credit Score Before Applying

Lenders reward good credit with better rates. If you have time before buying, focus on improving your score. This means paying down existing credit card balances and ensuring all current bills are paid on time. Check your report via ConsumerFinance.gov to spot errors.

Step 2: Maximize Your Down Payment

Every extra dollar saved up and put down directly lowers your loan principal immediately. If you can stretch your savings goal by two extra months to save $1,000 more, that can shave off a significant chunk of your monthly minimum.

Step 3: Target Shorter Loan Terms (If Possible)

While it seems counterintuitive because it raises the monthly payment, aiming for a 60-month loan instead of a 72-month loan will save you hundreds, sometimes thousands, in interest. If you can comfortably afford the 60-month payment, choose it!

Step 4: Shop Around for Financing

Never settle for the first rate offered by the dealership. Get pre-approved through your local credit union or bank first. Having a pre-approval letter gives you negotiating power. If the dealer can beat your bank’s rate, great! If not, you use your pre-approved loan.

Step 5: Consider A Lower Trim Level

If an EX is stretching the budget, look closely at the LX or Sport trims. Sometimes, the difference in features isn’t worth the extra $50 or $70 per month in borrowing costs, especially when factoring in tax and interest.

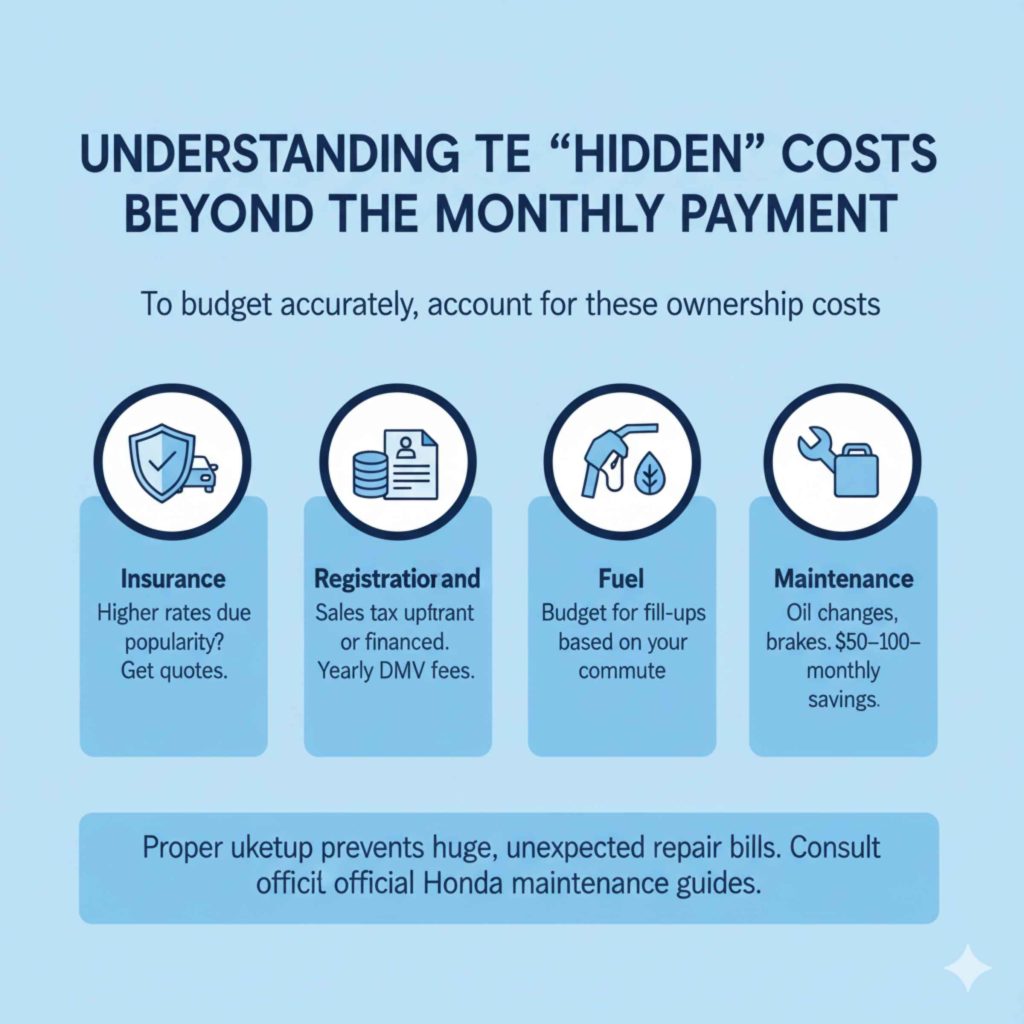

Understanding the “Hidden” Costs Beyond the Monthly Payment

As your trusted automotive guide, I must remind you that the monthly car payment isn’t the only expense associated with owning a Civic. To budget accurately, you need to account for these ownership costs.

- Insurance: Civics are one of the most popular cars, which can sometimes mean higher comprehensive insurance rates depending on your area and driving history. Get quotes before you buy.

- Registration and Taxes: Sales tax will be added to the financed amount (unless paid upfront). Registration fees are paid yearly or biennially to your state DMV.

- Fuel: While Civics are fuel-efficient, you still need to budget for regular fill-ups based on your daily commute.

- Maintenance: While reliable, Civics require regular oil changes, tire rotations, and eventual replacement items like brakes. Budget about $50–$100 monthly for future maintenance savings, even if you don’t use it right away.

For helpful, step-by-step maintenance schedules specific to various Civic model years, always consult the official Honda maintenance guides. Proper upkeep keeps your car running reliably and prevents huge, unexpected repair bills.

Frequently Asked Questions About Honda Civic Payments

Q1: Can I get a Honda Civic with no down payment?

Yes, many lenders offer 100% financing, but this means you are borrowing the entire cost of the car, plus taxes and fees. This results in a higher monthly payment and higher interest costs over the long run. It’s usually best to aim for at least $1,000 down if possible.

Q2: What credit score do I need for the best Civic financing rate?

Typically, buyers with credit scores of 740 or higher are considered “prime” or “super prime” and qualify for the lowest advertised rates offered by Honda Financial Services or banks. Scores below 620 will likely see much higher APRs.

Q3: How much more will a Civic Si cost per month than a base Civic LX?

A Civic Si usually costs about $3,000 to $4,000 more than the LX trim. This difference, financed over 60 months at the same rate, could add about $55 to $75 to your monthly payment.

Q4: Are Honda dealer incentives available that lower the payment?

Yes, manufacturers often offer special low APR financing (sometimes 0% or 0.9%) on current model years, especially at the end of the month or year. These incentives are fantastic because they drastically reduce the interest portion of your payment.

Q5: Does my trade-in affect my monthly payment?

Absolutely. If you trade in an old car, the equity (the amount you own it for minus the amount you still owe) is applied directly to the down payment of the new Civic. This reduces the principal and lowers your monthly payment significantly.

Q6: What is a realistic budget for a used Honda Civic payment?

If you are looking at a quality used Civic (3 to 5 years old) with a reasonable loan, you should realistically aim for a monthly payment falling between $300 and $400, depending on your down payment.

Conclusion: Confidence in Your Civic Budget

Figuring out how much is a car payment for a Honda Civic doesn’t have to be a guessing game. As we’ve seen, it truly comes down to four main levers: the price of the car, how much you put down, the length of the loan, and your personal interest rate. By focusing on securing the best possible interest rate through a strong credit history and maximizing your down payment, you gain direct control over making that payment fit comfortably into your life.

The Honda Civic remains an excellent, reliable choice for the long term. Use the scenarios we calculated as a benchmark for your own situation. Get pre-approved rates from a few different places, know your “Out-the-Door” price before stepping into the dealership, and you’ll walk away knowing you made a smart, confident financial decision for your new reliable ride.